Mario Seccareccia’s note last week did a great job of showing how the Summers/Krugman “liquidity trap” argument is just the old Wicksellian loanable funds market, which has acquired something like the status of a folk theorem in economics. “Within this neoclassical theoretical box”, the note states, “there is only one solution to move the economy out of secular stagnation. One must boost the Wicksellian “natural rate” by strengthening expectations of return.” This could be done, as the note argues and following Wicksellian logic, by a policy of negative real interest rates (amounting to a fiscal subsidy on borrowing) which might do the job of triggering an asset bubble.

What the note does not state so clearly, however, is that Wicksell assumed that the loanable funds market operates in a situation of full employment, i.e. income would be at the full employment level. The (natural) interest rate would then balance savings supply and investment demand, only affecting the composition (but not the level) of full-employment income. Keynes argued, of course, that it was possible for investment and saving to be equal at any level of income, which implies that the equilibrium rate of interest might be consistent with any amount of unemployment. Applying Wicksell’s loanable funds model in a blatantly non-full employment context, as Krugman and Summers are doing, is – therefore – a red herring, distracting attention from the real issue, which is: unemployment due to lack of demand.

Secondly, however perverse a monetary policy of negative real interest rates may be, I do think it is unlikely to have much of an impact in the current balance-sheet recession. The heavily-indebted private sector (mainly households) will take the credit (plus subsidy) to pay down its debts – yes, perhaps part of it will spill-over in higher asset prices (somewhere), but most will be used to reduce the debt overhang, without much impact on the real economy.

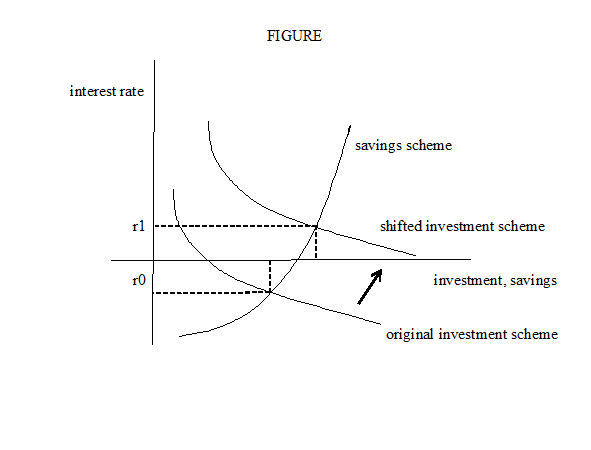

Now back to Summer’s and Krugman’s (faulty) Wicksellian logic. I am puzzled why they ignore the fiscal policy option. The position of the investment schedule (loanable funds demand) clearly depends upon the interest rate as well as the state of confidence of business investors. But it also depends on public investment. If public investment is stepped up, this raises the demand for loanable funds. With an unchanged loanable funds supply, the interest rate must go up, in the process crowding out interest-rate sensitive private-sector investment. New Consensus Economists never grew tired, back in the pre-crisis days, of pointing to the crowding-out impact of expanded public investment. But if it worked back then, it should also work now: any increase in public investment will push up the investment schedule (see FIGURE below) and this will help in raising the interest rate, increasing savings as well as aggregate investment – especially because (a) the savings scheme will be rather steeply increasing (people save out of the precautionary motive, and less in response to the interest rate); and (b) private investment will be overwhelmingly dependent upon a lack of confidence of the business investors (and less affected by the – low – interest rate).

Source

0 comments:

Post a Comment