Gold price collapse is the worst for 30 years ... The precious metal has been one of the worst-performing assets in 2013, bringing an end to a decade-long rally. Gold has fallen almost 28pc over the last 12 months ... Gold will finish the year as one of the worst-performing asset classes, bringing to an end a decade-long rally in the precious metal. Gold has suffered its sharpest fall in 30 years, down almost 28pc over the past 12 months to close 2013 at about $1,200 (£725) an ounce. – UK Telegraph Dominant

Social Theme: This silly yellow stuff simply doesn't perform.

Free-Market Analysis: There is no denying gold has fallen and hasn't yet gotten up. But the reasons for its failure and eventual resurgence remain intensely interesting.

Surely no logical person can doubt that the world's securities markets are manipulated. Would that it were not so, but it is. And very obviously, or so it seems to us, the manipulation is growing more severe.

But manipulations do not last forever. If the current price of currencies against gold does not represent a "true" price in the current market, then sooner or later the market will adjust the price.

One must visualize a kind of war going on between those who want to control the market and the many decisions of buyers and sellers that are determinedly interested in price discovery rather than a particular point of control.

Having pointed this out, we also must admit that currency price appreciation against gold has been considerable and this article does a good job of summarizing it.

Here's more:

Equities have won the battle over gold for investors' money this year," Ole Hansen, head of commodity strategy at Saxo Bank, said.

Last year, Mr Hansen correctly predicted that gold would finish the year at $1,200 and for 2014 he is forecasting that prices may have already bottomed out. ...

"A year down the line, we could be around $1,250 an ounce," he said. Demand for gold had led the charge in resources demand that became known as the commodities "super-cycle", but no longer.

Gold was the biggest loser after the US Federal Reserve announced that it will taper its bond purchases by $10bn a month from next year. The metal fell almost 3pc immediately after news of the taper hit the market.

Central banks globally are already following the Fed's lead and easing back on the money printing that has been the primary policy tool to lift the developed world out of recession, and a major factor behind investors seeking higher yields in gold.

"Sentiment is stacked against gold," said Mark Bristow, chief executive of African-focused gold mining company, Randgold Resources. "Globally, economic policy has been driven by popular politics and not sound business sense." Mr Bristow said that not all of the downward pressure on gold prices is due to global economic forces. Over-production is now a major problem, especially among miners operating on low margins.

This article cites over-production of gold as a key factor in currency appreciation against the yellow metal. And yet the ongoing reported lines of gold buyers in China and India provide us with an alternative reality, one that seems to contradict the oversupply argument.

We are told as well that the expansion of the Fed "taper" has put downward pressure on gold but the taper is a relative latecomer. Gold collapsed a while ago.

We are informed that the sell-off was merely a market phenomenon. Trees do not grow to the sky and after a decade of fairly steady decline in paper currencies relative to gold prices, it was time for a bit of paper price appreciation. Maybe, and yet we are not convinced ...

We note that gold price manipulation is now formally under investigation in London and that the price of gold is "set" by traders and banks rather than by the market. We are supposed to believe there is a technical reason for this, but there is none – except that "setting" prices is far more conducive to manipulation than observing and recording them.

We have seen as well that equity market manipulations are becoming more and more evident. We've called this the "Wall Street Party," and despite occasional shrill denunciations from alternative media pundits, we would tend to believe that the current equity market moves can continue upwards for some time, albeit with pauses, and severe or not-so-severe pullbacks.

Janet Yellen's bias toward money printing – which she will soon bring to the Federal Reserve's top job – generally low interest rates around the world, the fracking phenomenon that purports to provide the world with efficient and plentiful oil, and lower gold prices all contribute to a favorable outlook for stocks especially.

Sometimes when listing factors supporting this Wall Street Party phenomenon we forget to include the great gold route. But to speculate that the gold downturn was either generated or manipulated for purposes of boosting equities would not be especially rash within the larger frame of reference.

In any event, these basics abide; it is indeed reasonable to believe that if there is a larger bankers' plan to boost securities, especially stocks, paper price appreciation against gold will continue as well.

It is also wise to assume that the latest stock manipulation, as broad as it is, will not go on forever and thus at some point gold will again prove how it retains value against a slew of paper currencies including the dollar.

Conclusion

Paper appreciation against gold is just one more reason to conclude that there is at least a short-term stock manipulation being implemented. One cannot necessarily point to a "smoking gun," but the pattern reveals a motive that inevitably accompanies the reality.

Source

“Honey, I Shrunk Killed the Middle Class”

3:00 AM

No comments

A new Bloomberg story, Americans on Wrong Side of Income Gap Run Out of Means to Cope, is a zeitgeist indicator: the normally-well-insulated-from-realty investing classes have noticed that large swathes of what was once the middle class aren’t just downwardly mobile but are struggling. Some facts from the story:

So it may be that even as the stock market roars ahead, more investors are coming to recognize the shoddy foundations of this so-called recovery and perhaps more important, that the legitimacy of the ruling classes erodes quickly when ordinary citizens recognize how badly the deck is stacked against them. But the upper crust and the technocratic elites are sufficiently cloistered that it will take more than an article or two for them to recognize the mess they’ve created for their fellow citizens, and ultimately, themselves.

Source

The top 10 percent in the US captured a biggest share of income in 2012 than any year since 1917

Real median income of college-educated men 25 or older fell 10% since 2007

Of people who lost jobs in 2009 through 2011 that they’d had for three or more years, only half the women and 61% of the men were re-employed by the start of 2012 (and remember, a mere one paid hour of work a week counts as employment)

But the Bloomberg story find it hard to capture what this distress means in human terms. It does have this anecdote at the close:

Only 1/3 of adults 18 to 32 lived in their own household, only marginally higher than the 38 year low set in 2010

The growing calls for action to reduce income inequality have translated into a national push for a higher minimum wage. Fast-food workers in 100 cities took to the streets Dec. 5 to demand a $15 hourly salary.

Latoya Caldwell, 30, of Kansas City, Missouri, is among those who took part. She’s been employed at a Wendy’s Co. restaurant for six years and earns the state’s minimum wage of $7.35 an hour. Working 25 to 30 hours a week, she has asked for more shifts to help support her four children, with whom she lives in one bedroom of her aunt’s house.

More older workers — including one over 65 years — as well as college-educated are joining her team, showing that rough economic times have swelled the ranks beyond the typical teenager at the register, Caldwell said.

“We’re making barely enough to even survive,” Caldwell said. “We’re not even surviving — we’re dependent on state assistance while our CEO makes $5.8 million and he’s sitting in an office.”The nouveau pauvre are not much better off. I suspect some NC readers are feeling the pinch despite concerted efforts to live frugally. An email today had the subject line “Poverty is expensive”:

My expenses are beginning to get the better of me and month’s end is stretching beyond my dollars. Next year is looking the same. So, yesterday I was pointedly reminded how expensive it is to be poor. Instead of buying a lot when something I use is on sale, I have to buy what I have dollars for. No savings for me! And instead of buying by unit price–I’m a ferocious unit price shopper–I have to buy whatever size I have dollars for. And now I have to make more trips because I can only buy small dollars worth at a time.

Being poor is MUCH more expensive than being not poor. Not even wealthy, just not poor. Back in the day when there were two kids in the house, I bought detergent on sale, saved $10.00 per buy, and had detergent for months and months. Any sale of stuff I used I snarfed up a bunch. Makes a difference just in trips to the store. We tried to keep wkly shopping to the perishables and we pretty well succeeded. Sometimes went to DE for taxable items and calculated so the trip, gas and bridge toll, was worth it: loaded the car and considered a sale a small gold mine.

Can’t do that anymore. I don’t need eight gallons of detergent anyway, but even smaller lots are beyond my cash means. Does anyone who matters in economics realize how expensive being poor is? I think some do and most don’t care. Not their problem. I do so wish it were.The one wee bit of good news in the Bloomberg account is that things have gotten so bad that pundits and politicians are starting to make noise about the destruction of the middle class, which is a necessary but far from sufficient condition for change. For instance:

“The middle has really collapsed,” said Lawrence Katz, an economics professor at Harvard University in Cambridge, Massachusetts, and a former chief economist at the Labor Department in Washington….

“Wall Street is roaring and Main Street is struggling,” Representative Kevin Brady, a Texas Republican and chairman of the Joint Economic Committee, said in an interview. “Quantitative easing has really exacerbated income inequality.”The Brady quote and others in the article show that the Republicans are looking to get mileage from the increase in income inequality under Obama, which was greater than that under Bush. There’s a reveling lack of defenses for the President’s policies. And the Fed isn’t too convincing either:

Janet Yellen, nominated to take over as Fed chairman next year, defended the central bank’s actions at a Senate Banking Committee hearing on Nov. 14.

“The policies we’ve undertaken have been meant to generate a robust recovery,” Yellen told the committee.Oh, puhleeze. Robust recovery for who? The Fed not only threw staggering amounts of firepower at salvaging bank balance sheets, while showing no interest in rescuing ordinary Americans. It was also all-in on the Administration’s program to paper over the banks’ chain of title problems and their widespread servicing abuses, and didn’t bother to obtain any meaningful concessions or reforms, the most important of which would have been principal modifications, a remedy favored by investors as well as homeowners. The Fed has been all too happy to accept mission creep rather than speak up forcefully for the need for more fiscal stimulus.

So it may be that even as the stock market roars ahead, more investors are coming to recognize the shoddy foundations of this so-called recovery and perhaps more important, that the legitimacy of the ruling classes erodes quickly when ordinary citizens recognize how badly the deck is stacked against them. But the upper crust and the technocratic elites are sufficiently cloistered that it will take more than an article or two for them to recognize the mess they’ve created for their fellow citizens, and ultimately, themselves.

Source

The Stock Market Has Officially Entered Crazytown Territory

2:06 AM

No comments

It is time to crank up the Looney Tunes theme song because Wall Street has officially entered crazytown territory. Stocks just keep going higher and higher, and at this point what is happening in the stock market does not bear any resemblance to what is going on in the overall economy whatsoever. So how long can this irrational state of affairs possibly continue? Stocks seem to go up no matter what happens. If there is good news, stocks go up. If there is bad news, stocks go up. If there is no news, stocks go up. On Thursday, the day after Christmas, the Dow was up another 122 points to another new all-time record high. In fact, the Dow has had an astonishing 50 record high closes this year. This reminds me of the kind of euphoria that we witnessed during the peak of the housing bubble. At the time, housing prices just kept going higher and higher and everyone rushed to buy before they were "priced out of the market". But we all know how that ended, and this stock market bubble is headed for a similar ending.

It is almost as if Wall Street has not learned any lessons from the last two major stock market crashes at all. Just look at Twitter. At the current price, Twitter is supposedly worth 40.7 BILLION dollars. But Twitter is not profitable. It is a seven-year-old company that has never made a single dollar of profit.

Not one single dollar.

In fact, Twitter actually lost 64.6 million dollars last quarter alone. And Twitter is expected to continue losing money for all of 2015 as well.

But Twitter stock is up 82 percent over the last 30 days, and nobody can really give a rational reason for why this is happening.

Overall, the Dow is up more than 25 percent so far this year. Unless something really weird happens over the next few days, it will be the best year for the Dow since 1996.

It has been a wonderful run for Wall Street. Unfortunately, there are a whole host of signs that we have entered very dangerous territory.

The median price-to-earnings ratio on the S&P 500 has reached an all-time record high, and margin debt at the New York Stock Exchange has reached a level that we have never seen before. In other words, stocks are massively overpriced and people have been borrowing huge amounts of money to buy stocks. These are behaviors that we also saw just before the last two stock market bubbles burst.

And of course the most troubling sign is that even as the stock market soars to unprecedented heights, the state of the overall U.S. economy is actually getting worse...

-During the last full week before Christmas, U.S. store visits were 21 percent lower than a year earlier and retail sales were 3.1 percent lower than a year earlier.

-The number of mortgage applications just hit a new 13 year low.

-The yield on 10 year U.S. Treasuries just hit 3 percent.

For many more signs like this, please see my previous article entitled "37 Reasons Why 'The Economic Recovery Of 2013' Is A Giant Lie".

And most Americans don't realize this, but the U.S. financial system and the overall U.S. economy are now in much weaker condition than they were the last time we had a major financial crash back in 2008.

Employment is at a much lower level than it was back then and our banking system is much more vulnerable than it was back then. Just before the last financial crash, the U.S. national debt was sitting at about 10 trillion dollars, but today it has risen to more than 17.2 trillion dollars. The following excerpt from a recent article posted on thedailycrux.com contains even more facts and figures which show how our "balance sheet numbers" continue to get even worse...

Just because a bunch of half-crazed investors are going into massive amounts of debt in a desperate attempt to make a quick buck does not mean that the overall economy is in good shape.

In fact, much of the country is in such rough shape that "reverse shopping" has become a huge trend. Even big corporations such as McDonald's are urging their employees to return their Christmas gifts in order to bring in some much needed money...

It is almost as if Wall Street has not learned any lessons from the last two major stock market crashes at all. Just look at Twitter. At the current price, Twitter is supposedly worth 40.7 BILLION dollars. But Twitter is not profitable. It is a seven-year-old company that has never made a single dollar of profit.

Not one single dollar.

In fact, Twitter actually lost 64.6 million dollars last quarter alone. And Twitter is expected to continue losing money for all of 2015 as well.

But Twitter stock is up 82 percent over the last 30 days, and nobody can really give a rational reason for why this is happening.

Overall, the Dow is up more than 25 percent so far this year. Unless something really weird happens over the next few days, it will be the best year for the Dow since 1996.

It has been a wonderful run for Wall Street. Unfortunately, there are a whole host of signs that we have entered very dangerous territory.

The median price-to-earnings ratio on the S&P 500 has reached an all-time record high, and margin debt at the New York Stock Exchange has reached a level that we have never seen before. In other words, stocks are massively overpriced and people have been borrowing huge amounts of money to buy stocks. These are behaviors that we also saw just before the last two stock market bubbles burst.

And of course the most troubling sign is that even as the stock market soars to unprecedented heights, the state of the overall U.S. economy is actually getting worse...

-During the last full week before Christmas, U.S. store visits were 21 percent lower than a year earlier and retail sales were 3.1 percent lower than a year earlier.

-The number of mortgage applications just hit a new 13 year low.

-The yield on 10 year U.S. Treasuries just hit 3 percent.

For many more signs like this, please see my previous article entitled "37 Reasons Why 'The Economic Recovery Of 2013' Is A Giant Lie".

And most Americans don't realize this, but the U.S. financial system and the overall U.S. economy are now in much weaker condition than they were the last time we had a major financial crash back in 2008.

Employment is at a much lower level than it was back then and our banking system is much more vulnerable than it was back then. Just before the last financial crash, the U.S. national debt was sitting at about 10 trillion dollars, but today it has risen to more than 17.2 trillion dollars. The following excerpt from a recent article posted on thedailycrux.com contains even more facts and figures which show how our "balance sheet numbers" continue to get even worse...

{kind=link}

Since the fourth quarter of 2009, the U.S. current account deficit has been more than $100 billion per quarter. As a result, foreigners now own $4.2 trillion more U.S. investment assets than we own abroad. That's $1.7 trillion more than when Buffett first warned about this huge problem in 2003. Said another way, the problem is 68% bigger now.

And here's a number no one else will tell you – not even Buffett. Foreigners now own $25 trillion in U.S. assets. And yet… we continue to consume far more than we produce, and we borrow massively to finance our deficits.

Since 2007, the total government debt in the U.S. (federal, state, and local) has doubled from around $10 trillion to $20 trillion.

Meanwhile, the size of Fannie and Freddie's mortgage book declined slightly since 2007, falling from $4.9 trillion to $4.6 trillion. That's some good news, right?

Nope. The excesses just moved to a new agency. The "other" federal mortgage bank, the Federal Housing Administration, now is originating 20% of all mortgages in the U.S., up from less than 5% in 2007.

Student debt, also spurred on by government guarantees, has also boomed, doubling since 2007 to more than $1 trillion. Altogether, total debt in our economy has grown from around $50 trillion to more than $60 trillion since 2007.So don't be fooled by this irrational stock market bubble.

Just because a bunch of half-crazed investors are going into massive amounts of debt in a desperate attempt to make a quick buck does not mean that the overall economy is in good shape.

In fact, much of the country is in such rough shape that "reverse shopping" has become a huge trend. Even big corporations such as McDonald's are urging their employees to return their Christmas gifts in order to bring in some much needed money...

In a stark reminder of how tough things still are for low-income families in America, McDonalds has advised workers to dig themselves "out of holiday debt" by cashing in their Christmas haul."You may want to consider returning some of your unopened purchases that may not seem as appealing as they did," said a website set up for employees.

"Selling some of your unwanted possessions on eBay or Craigslist could bring in some quick cash."This irrational stock market bubble is not going to last for too much longer. And a lot of top financial experts are now warning their clients to prepare for the worst. For example, David John Marotta of Marotta Wealth Management recently told his clients that they should all have a "bug-out bag" that contains food, a gun and some ammunition...

A top financial advisor, worried that Obamacare, the NSA spying scandal and spiraling national debt is increasing the chances for a fiscal and social disaster, is recommending that Americans prepare a “bug-out bag” that includes food, a gun and ammo to help them stay alive.

David John Marotta, a Wall Street expert and financial advisor and Forbes contributor, said in a note to investors, “Firearms are the last item on the list, but they are on the list. There are some terrible people in this world. And you are safer when your trusted neighbors have firearms.”

His memo is part of a series addressing the potential for a “financial apocalypse.” His view, however, is that the problems plaguing the country won't result in armageddon. “There is the possibility of a precipitous decline, although a long and drawn out malaise is much more likely,” said the Charlottesville, Va.-based president of Marotta Wealth Management.Source

Now China ... Reasons for Printing Money Abound

3:35 AM

No comments

China move calms credit concerns ... Chinese authorities have been trying to curb excessive lending ... China's central bank has pumped $5bn (£3.1bn) into the banking system to ease concerns over a credit squeeze that has caused rising interest rates. The People's Bank of China did not explain its actions, but over the last few days there has been growing concern over the availability of credit. That has been reflected in the interest rates banks charge each other. – BBC

Dominant Social Theme: The economy is perched on a precipice. Let's stimulate. We've stimulated too much. Let's stop. Well, let's slow down anyway. The markets are doing fine.

Free-Market Analysis: Every central bank of note in the world is printing money faster and faster. We don't think this is any coincidence. The world's top bankers seem to want a huge stock market explosion that will make current averages look fairly tame.

What comes after the punch bowl is taken away is a deeply concerning question. But don't think about that now. Just let the good times roll!

This is a Wall Street Party to end all such parties. And you can watch those behind this particular sub-dominant social theme justify it any one of a number of ways.

In Japan, the government suddenly started printing money because it is a new one with "new ideas."

In England, the BOE still prints money in great gouts, and BOE governor Mark Carney has utilized the new "tool" of forward guidance to assure interested parties that the BOE intends to continue its easy money policy for as long as necessary.

In the US, the Fed is supposed to be slowing money printing with a "tapering," but this is a highly questionable pull-back, as Fed officials have signaled, at the same time, that they have no intention of letting markets deflate.

In China, as we can see above, the central bank is once again engaged in a money-printing exercise. We've mentioned these four central banks because, so far as we can tell, their managers control the better part of 75 percent of the world's money supply. And all of these central banks are printing. In mid-2013, the UK Guardian reported on this phenomenon as follows:

In its annual report, published on Sunday, the Bank for International Settlements based in Basle, Switzerland, warns that with unprecedented stimulus already in place, fresh action from central banks to kick-start growth may do more harm than good, by distorting financial markets and jeopardising stability.

"Unfortunately, central banks cannot do more without compounding the risks they have already created. Monetary stimulus alone cannot put economies on a path to robust, self-sustaining growth, because the roots of the problem preventing such growth are not monetary," said Stephen Cecchetti, head of the bank's monetary and economic department, presenting the report.

And yet the madness continues. Here's more from the BBC article we excerpted above:

On Monday one important benchmark rate rose to its highest level since June, the height of China's credit crunch. The seven day bond repurchase rate hit 8.93% but fell back to 6.56% after the central bank added funds to the banking system.

Analysts are blaming China's current cash crunch on a number of factors. In a process known as "window dressing" banks typically conserve cash at the end of the year to keep their balance sheets looking healthy. However this year they have been doing that in a different financial environment.

Chinese authorities have been trying to discourage excessive lending by curbing official credit lines and slowing government spending. "The banks are being forced to adapt to regulatory changes - so they are being forced to hold additional capital. Banks that have been used to operating on very easy and loose conditions are now finding that those conditions are starting tighten," said Jeremy Stretch, market strategist at CIBC.

"Authorities are fearing that this is causing a scramble for cash and that is pushing up the rates and so they are being forced to inject some money into the system," he said. In June banks suffered a more serious credit squeeze and the benchmark interbank lending rate jumped to a record 13.4%.

The window dressing is actually being constructed by central bankers themselves in conjunction with the mainstream media. The idea seems to be that central bankers do not want to be too clear about their plans.

The mainstream media is constantly sounding concerns about the looseness of money, and lately, in the West the financial reporting has focused relentlessly on tapering – which simply means that the US Fed will purchase fewer government bonds.

But, in fact, the US central bank along with the other big ones referred to above is not REALLY reducing money flows a great deal.

The tightening talk we're listening to is just for public consumption. The whole system of recovery is based on equity appreciation stimulating employment (which it does ineffectively at best). But if top Western bankers seek this sort of recovery, stimulate they must.

And they are.

Constantly, we hear they are not. But they are. Always, they are.

The big central banks around the world are all pumping money in unison. The media continues to write about "tightening."

What is being planned are higher market highs. We will always be told that bankers are concernedly moderating money flows. But then, at the first sign of trouble, the taps are turned back on.

In fact, they are never REALLY turned off. And there will always be a reason to push the volume of money even higher.

They are planning a big Wall Street Party. The top men always seem to find reasons to print more. Until the world is swimming in currency.

Conclusion That's the plan, or so it seems.

Source

Dominant Social Theme: The economy is perched on a precipice. Let's stimulate. We've stimulated too much. Let's stop. Well, let's slow down anyway. The markets are doing fine.

Free-Market Analysis: Every central bank of note in the world is printing money faster and faster. We don't think this is any coincidence. The world's top bankers seem to want a huge stock market explosion that will make current averages look fairly tame.

What comes after the punch bowl is taken away is a deeply concerning question. But don't think about that now. Just let the good times roll!

This is a Wall Street Party to end all such parties. And you can watch those behind this particular sub-dominant social theme justify it any one of a number of ways.

In Japan, the government suddenly started printing money because it is a new one with "new ideas."

In England, the BOE still prints money in great gouts, and BOE governor Mark Carney has utilized the new "tool" of forward guidance to assure interested parties that the BOE intends to continue its easy money policy for as long as necessary.

In the US, the Fed is supposed to be slowing money printing with a "tapering," but this is a highly questionable pull-back, as Fed officials have signaled, at the same time, that they have no intention of letting markets deflate.

In China, as we can see above, the central bank is once again engaged in a money-printing exercise. We've mentioned these four central banks because, so far as we can tell, their managers control the better part of 75 percent of the world's money supply. And all of these central banks are printing. In mid-2013, the UK Guardian reported on this phenomenon as follows:

In its annual report, published on Sunday, the Bank for International Settlements based in Basle, Switzerland, warns that with unprecedented stimulus already in place, fresh action from central banks to kick-start growth may do more harm than good, by distorting financial markets and jeopardising stability.

"Unfortunately, central banks cannot do more without compounding the risks they have already created. Monetary stimulus alone cannot put economies on a path to robust, self-sustaining growth, because the roots of the problem preventing such growth are not monetary," said Stephen Cecchetti, head of the bank's monetary and economic department, presenting the report.

And yet the madness continues. Here's more from the BBC article we excerpted above:

On Monday one important benchmark rate rose to its highest level since June, the height of China's credit crunch. The seven day bond repurchase rate hit 8.93% but fell back to 6.56% after the central bank added funds to the banking system.

Analysts are blaming China's current cash crunch on a number of factors. In a process known as "window dressing" banks typically conserve cash at the end of the year to keep their balance sheets looking healthy. However this year they have been doing that in a different financial environment.

Chinese authorities have been trying to discourage excessive lending by curbing official credit lines and slowing government spending. "The banks are being forced to adapt to regulatory changes - so they are being forced to hold additional capital. Banks that have been used to operating on very easy and loose conditions are now finding that those conditions are starting tighten," said Jeremy Stretch, market strategist at CIBC.

"Authorities are fearing that this is causing a scramble for cash and that is pushing up the rates and so they are being forced to inject some money into the system," he said. In June banks suffered a more serious credit squeeze and the benchmark interbank lending rate jumped to a record 13.4%.

The window dressing is actually being constructed by central bankers themselves in conjunction with the mainstream media. The idea seems to be that central bankers do not want to be too clear about their plans.

The mainstream media is constantly sounding concerns about the looseness of money, and lately, in the West the financial reporting has focused relentlessly on tapering – which simply means that the US Fed will purchase fewer government bonds.

But, in fact, the US central bank along with the other big ones referred to above is not REALLY reducing money flows a great deal.

The tightening talk we're listening to is just for public consumption. The whole system of recovery is based on equity appreciation stimulating employment (which it does ineffectively at best). But if top Western bankers seek this sort of recovery, stimulate they must.

And they are.

Constantly, we hear they are not. But they are. Always, they are.

The big central banks around the world are all pumping money in unison. The media continues to write about "tightening."

What is being planned are higher market highs. We will always be told that bankers are concernedly moderating money flows. But then, at the first sign of trouble, the taps are turned back on.

In fact, they are never REALLY turned off. And there will always be a reason to push the volume of money even higher.

They are planning a big Wall Street Party. The top men always seem to find reasons to print more. Until the world is swimming in currency.

Conclusion That's the plan, or so it seems.

Source

Wolf Richter: Financial Engineering Wildest Since The 2007 Bubble

4:20 AM

1 comment

Financial engineering had a glorious year in 2013. The last time we had this much crazy fun had been in 2007. Back then, Merger Mondays were hot on CNBC. Deals, no matter how large and how insanely leveraged, were announced with great hoopla. Rational people were seen shaking their heads at incongruous moments. Stocks were defying gravity. That was the last time we had this much fun because the bubble collapsed, and some of its detritus was skillfully heaped on the Fed’s balance sheet or on the taxpayer’s shoulders.

But now finally, after five years, the crazy fun is back, and the good thing is: this time, it’s different. This time, the smart money is selling!

In total, 229 IPOs were priced in the US in 2013, up 58% from last year, raising $61.3 billion, the highest amount since 2007, according to Dealogic. Stocks of companies that went public this year saw their prices soar on average 61.6%, compared to the already dizzying 38% of the Russell 2000 Growth index and the 27% of the S&P 500 (Renaissance Capital, chart).

In terms of dollars raised – not hype generated – the largest deal was Houston-based pipeline outfit Plains GP Holdings LP, which raised $2.9 billion in October. Who was selling? The smart money! Among them, Occidental Petroleum, The Energy and Minerals Group, Kayne Anderson Capital Advisors, and of course the smartest of them all, the executives.

Hilton’s IPO, which raised $2.7 billion in December, was in second place. Blackstone had taken Hilton private during the LBO frenzy in 2007 in a mind-bendingly leveraged deal for $26.7 billion, including debt. For how this came about, read David Stockman’s trenchant and scathing analysis: Bernanke’s (Untough) Love Child: The $27 Billion Affair at the Hilton.

Pfizer unloaded animal-medicine subsidiary Zoetis in January, raising $2.2 billion. In fourth place, finally a Silicon Valley hero, and certainly number one in hype, Twitter. It still hasn’t figured out how to make money, but it raised 2.1 billion. Natural gas driller Antero Resources, controlled by Warburg Pincus, raised $1.8 billion.

It was a huge year for IPOs. We knew it would be. We’ve been informed. “We’re selling everything that’s not nailed down,” explained Leon Black, CEO of private equity giant Apollo Global Management back in April. The smart money has been busy doing that. And not just through IPOs….

Global junk-bond issuance rose 12% from last year, to an all-time high of $477 billion. It was powered by veritable frenzy in Europe where deal volume surged 54% to $122 billion. In the US, the taper tantrum over the summer caused junk bonds to dive, a harbinger for things to come when the Fed actually stops buying bonds, rather than just talk about it. In May, it still looked like a record year. But with turmoil rippling across that space over the summer, volume for the year dropped 6% to 260 billion, from last year’s all time high of $275 billion.

Who made the big bickies, as my friends from down under might say? Card-carrying financial engineers. In the US, investment banking fees rose 12% to $36 billion, about matching the previous record set during the bubble of 2007. In Europe, fees rose 10% to 18 billion.

But there was a fly in the ointment. Asia Pacific had its worst year since the crisis of 2008. That includes Japan despite its money-printing binge whose magnitude trumped anything that even the Fed in its reckless splendor has dared to do. While M&A dollar volume rose 11% due to some large deals in China, activity fell 12% to the lowest number of deals since 2006. Volume in the debt capital markets plunged 15%.

There was another problem in Asia: competition. Banks that had piled into the space competed ferociously, which put downward pressure on fees. So, investment banking revenues dropped 10% to $11.7 billion – a grizzly 26% below the peak year of 2010.

Despite the debacle in Asia, global investment banking fees rose to $73 billion. And that too was the highest since the bubble year 2007, when investment banks pocketed $90 billion. Think of how much more fun could have been had if Asia hadn’t dilly-dallied around.

And who got the lion’s share of these fees? JP Morgan gobbled up 8.6% globally and Bank of America Merrill Lynch 7.5%. They were followed by Goldman Sachs, Morgan Stanley, and Citigroup. For the first time since 2009, the global top five were our too-big-to-fail friends on Wall Street. The top ten were rounded out by Deutsche Bank, Credit Suisse, Barclays, Wells Fargo, and UBS.

They’re all celebrating their phenomenal success in extracting massive fees from a wheezing economy that has been barely wobbling along. But it’s also a warning signal: Financial engineering looks good on paper for a while, and the markets love it, and the hoopla makes everyone feel energized, especially those who take the cream off the top, and it feeds off the nearly free money the Feds hands to Wall Street. But after these financial engineers are done extracting fees and altering the landscape, they move on, leaving behind iffy debt, shares of dubious value, wildly growing tangles of risk, and other detritus. And a lot of these financially over-engineered constructs won’t make it in an environment where money isn’t free anymore.

Source

But now finally, after five years, the crazy fun is back, and the good thing is: this time, it’s different. This time, the smart money is selling!

In total, 229 IPOs were priced in the US in 2013, up 58% from last year, raising $61.3 billion, the highest amount since 2007, according to Dealogic. Stocks of companies that went public this year saw their prices soar on average 61.6%, compared to the already dizzying 38% of the Russell 2000 Growth index and the 27% of the S&P 500 (Renaissance Capital, chart).

In terms of dollars raised – not hype generated – the largest deal was Houston-based pipeline outfit Plains GP Holdings LP, which raised $2.9 billion in October. Who was selling? The smart money! Among them, Occidental Petroleum, The Energy and Minerals Group, Kayne Anderson Capital Advisors, and of course the smartest of them all, the executives.

Hilton’s IPO, which raised $2.7 billion in December, was in second place. Blackstone had taken Hilton private during the LBO frenzy in 2007 in a mind-bendingly leveraged deal for $26.7 billion, including debt. For how this came about, read David Stockman’s trenchant and scathing analysis: Bernanke’s (Untough) Love Child: The $27 Billion Affair at the Hilton.

Pfizer unloaded animal-medicine subsidiary Zoetis in January, raising $2.2 billion. In fourth place, finally a Silicon Valley hero, and certainly number one in hype, Twitter. It still hasn’t figured out how to make money, but it raised 2.1 billion. Natural gas driller Antero Resources, controlled by Warburg Pincus, raised $1.8 billion.

It was a huge year for IPOs. We knew it would be. We’ve been informed. “We’re selling everything that’s not nailed down,” explained Leon Black, CEO of private equity giant Apollo Global Management back in April. The smart money has been busy doing that. And not just through IPOs….

Global junk-bond issuance rose 12% from last year, to an all-time high of $477 billion. It was powered by veritable frenzy in Europe where deal volume surged 54% to $122 billion. In the US, the taper tantrum over the summer caused junk bonds to dive, a harbinger for things to come when the Fed actually stops buying bonds, rather than just talk about it. In May, it still looked like a record year. But with turmoil rippling across that space over the summer, volume for the year dropped 6% to 260 billion, from last year’s all time high of $275 billion.

Who made the big bickies, as my friends from down under might say? Card-carrying financial engineers. In the US, investment banking fees rose 12% to $36 billion, about matching the previous record set during the bubble of 2007. In Europe, fees rose 10% to 18 billion.

But there was a fly in the ointment. Asia Pacific had its worst year since the crisis of 2008. That includes Japan despite its money-printing binge whose magnitude trumped anything that even the Fed in its reckless splendor has dared to do. While M&A dollar volume rose 11% due to some large deals in China, activity fell 12% to the lowest number of deals since 2006. Volume in the debt capital markets plunged 15%.

There was another problem in Asia: competition. Banks that had piled into the space competed ferociously, which put downward pressure on fees. So, investment banking revenues dropped 10% to $11.7 billion – a grizzly 26% below the peak year of 2010.

Despite the debacle in Asia, global investment banking fees rose to $73 billion. And that too was the highest since the bubble year 2007, when investment banks pocketed $90 billion. Think of how much more fun could have been had if Asia hadn’t dilly-dallied around.

And who got the lion’s share of these fees? JP Morgan gobbled up 8.6% globally and Bank of America Merrill Lynch 7.5%. They were followed by Goldman Sachs, Morgan Stanley, and Citigroup. For the first time since 2009, the global top five were our too-big-to-fail friends on Wall Street. The top ten were rounded out by Deutsche Bank, Credit Suisse, Barclays, Wells Fargo, and UBS.

They’re all celebrating their phenomenal success in extracting massive fees from a wheezing economy that has been barely wobbling along. But it’s also a warning signal: Financial engineering looks good on paper for a while, and the markets love it, and the hoopla makes everyone feel energized, especially those who take the cream off the top, and it feeds off the nearly free money the Feds hands to Wall Street. But after these financial engineers are done extracting fees and altering the landscape, they move on, leaving behind iffy debt, shares of dubious value, wildly growing tangles of risk, and other detritus. And a lot of these financially over-engineered constructs won’t make it in an environment where money isn’t free anymore.

Source

On The 100th Anniversary Of The Federal Reserve Here Are 100 Reasons To Shut It Down Forever

2:58 AM

No comments

December 23rd, 1913 is a date which will live in infamy. That was the day when the Federal Reserve Act was pushed through Congress. Many members of Congress were absent that day, and the general public was distracted with holiday preparations. Now we have reached the 100th anniversary of the Federal Reserve, and most Americans still don't know what it actually is or how it functions. But understanding the Federal Reserve is absolutely critical, because the Fed is at the very heart of our economic problems. Since the Federal Reserve was created, there have been 18 recessions or depressions, the value of the U.S. dollar has declined by 98 percent, and the U.S. national debt has gotten more than 5000 times larger. This insidious debt-based financial system has literally made debt slaves out of all of us, and it is systematically destroying the bright future that our children and our grandchildren were supposed to have. If nothing is done, we are inevitably heading for a massive amount of economic pain as a nation. So please share this article with as many people as you can. The following are 100 reasons why the Federal Reserve should be shut down forever...

#1 We like to think that we have a government "of the people, by the people, for the people", but the truth is that an unelected, unaccountable group of central planners has far more power over our economy than anyone else in our society does.

#2 The Federal Reserve is actually "independent" of the government. In fact, the Federal Reserve has argued vehemently in federal court that it is "not an agency" of the federal government and therefore not subject to the Freedom of Information Act.

#3 The Federal Reserve openly admits that the 12 regional Federal Reserve banks are organized "much like private corporations".

#4 The regional Federal Reserve banks issue shares of stock to the "member banks" that own them.

#5 100% of the shareholders of the Federal Reserve are private banks. The U.S. government owns zero shares.

#6 The Federal Reserve is not an agency of the federal government, but it has been given power to regulate our banks and financial institutions. This should not be happening.

#7 According to Article I, Section 8 of the U.S. Constitution, the U.S. Congress is the one that is supposed to have the authority to "coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures". So why is the Federal Reserve doing it?

#8 If you look at a "U.S. dollar", it actually says "Federal Reserve note" at the top. In the financial world, a "note" is an instrument of debt.

#9 In 1963, President John F. Kennedy issued Executive Order 11110 which authorized the U.S. Treasury to issue "United States notes" which were created by the U.S. government directly and not by the Federal Reserve. He was assassinated shortly thereafter.

#10 Many of the debt-free United States notes issued under President Kennedy are still in circulation today.

#11 The Federal Reserve determines what levels some of the most important interest rates in our system are going to be set at. In a free market system, the free market would determine those interest rates.

#12 The Federal Reserve has become so powerful that it is now known as "the fourth branch of government".

#13 The greatest period of economic growth in U.S. history was when there was no central bank.

#14 The Federal Reserve was designed to be a perpetual debt machine. The bankers that designed it intended to trap the U.S. government in a perpetual debt spiral from which it could never possibly escape. Since the Federal Reserve was established 100 years ago, the U.S. national debt has gotten more than 5000 times larger.

#15 A permanent federal income tax was established the exact same year that the Federal Reserve was created. This was not a coincidence. In order to pay for all of the government debt that the Federal Reserve would create, a federal income tax was necessary. The whole idea was to transfer wealth from our pockets to the federal government and from the federal government to the bankers.

#16 The period prior to 1913 (when there was no income tax) was the greatest period of economic growth in U.S. history.

#17 Today, the U.S. tax code is about 13 miles long.

#18 From the time that the Federal Reserve was created until now, the U.S. dollar has lost 98 percent of its value.

#19 From the time that President Nixon took us off the gold standard until now, the U.S. dollar has lost 83 percent of its value.

#20 During the 100 years before the Federal Reserve was created, the U.S. economy rarely had any problems with inflation. But since the Federal Reserve was established, the U.S. economy has experienced constant and never ending inflation.

#21 In the century before the Federal Reserve was created, the average annual rate of inflation was about half a percent. In the century since the Federal Reserve was created, the average annual rate of inflation has been about 3.5 percent.

#22 The Federal Reserve has stripped the middle class of trillions of dollars of wealth through the hidden tax of inflation.

#23 The size of M1 has nearly doubled since 2008 thanks to the reckless money printing that the Federal Reserve has been doing.

#24 The Federal Reserve has been starting to behave like the Weimar Republic, and we all remember how that ended.

#25 The Federal Reserve has been consistently lying to us about the level of inflation in our economy. If the inflation rate was still calculated the same way that it was back when Jimmy Carter was president, the official rate of inflation would be somewhere between 8 and 10 percent today.

#26 Since the Federal Reserve was created, there have been 18 distinct recessions or depressions: 1918, 1920, 1923, 1926, 1929, 1937, 1945, 1949, 1953, 1958, 1960, 1969, 1973, 1980, 1981, 1990, 2001, 2008.

#27 Within 20 years of the creation of the Federal Reserve, the U.S. economy was plunged into the Great Depression.

#28 The Federal Reserve created the conditions that caused the stock market crash of 1929, and even Ben Bernanke admits that the response by the Fed to that crisis made the Great Depression even worse than it should have been.

#29 The "easy money" policies of former Fed Chairman Alan Greenspan set the stage for the great financial crisis of 2008.

#30 Without the Federal Reserve, the "subprime mortgage meltdown" would probably never have happened.

#31 If you can believe it, there have been 10 different economic recessions since 1950. The Federal Reserve created the "dotcom bubble", the Federal Reserve created the "housing bubble" and now it has created the largest bond bubble in the history of the planet.

#32 According to an official government report, the Federal Reserve made 16.1 trillion dollars in secret loans to the big banks during the last financial crisis. The following is a list of loan recipients that was taken directly from page 131 of the report...

Citigroup - $2.513 trillion

Morgan Stanley - $2.041 trillion

Merrill Lynch - $1.949 trillion

Bank of America - $1.344 trillion

Barclays PLC - $868 billion

Bear Sterns - $853 billion

Goldman Sachs - $814 billion

Royal Bank of Scotland - $541 billion

JP Morgan Chase - $391 billion

Deutsche Bank - $354 billion

UBS - $287 billion

Credit Suisse - $262 billion

Lehman Brothers - $183 billion

Bank of Scotland - $181 billion

BNP Paribas - $175 billion

Wells Fargo - $159 billion

Dexia - $159 billion

Wachovia - $142 billion

Dresdner Bank - $135 billion

Societe Generale - $124 billion

"All Other Borrowers" - $2.639 trillion

#33 The Federal Reserve also paid those big banks $659.4 million in "fees" to help "administer" those secret loans.

#34 During the last financial crisis, big European banks were allowed to borrow an "unlimited" amount of money from the Federal Reserve at ultra-low interest rates.

#35 The "easy money" policies of Federal Reserve Chairman Ben Bernanke have created the largest financial bubble this nation has ever seen, and this has set the stage for the great financial crisis that we are rapidly approaching.

#36 Since late 2008, the size of the Federal Reserve balance sheet has grown from less than a trillion dollars to more than 4 trillion dollars. This is complete and utter insanity.

#37 During the quantitative easing era, the value of the financial securities that the Fed has accumulated is greater than the total amount of publicly held debt that the U.S. government accumulated from the presidency of George Washington through the end of the presidency of Bill Clinton.

#38 Overall, the Federal Reserve now holds more than 32 percent of all 10 year equivalents, and that percentage is rising by about 0.3 percent each week.

#39 Quantitative easing creates financial bubbles, and when quantitative easing ends those bubbles tend to deflate rapidly.

#40 Most of the new money created by quantitative easing has ended up in the hands of the very wealthy.

#41 According to a prominent Federal Reserve insider, quantitative easing has been one giant "subsidy" for Wall Street banks.

#42 As one CNBC article recently stated, we are seeing absolutely rampant inflation in "stocks and bonds and art and Ferraris".

#43 Donald Trump once made the following statement about quantitative easing: "People like me will benefit from this."

#44 Most people have never heard about this, but a very interesting study conducted for the Bank of England shows that quantitative easing actually increases the gap between the wealthy and the poor.

#45 The gap between the top one percent and the rest of the country is now the greatest that it has been since the 1920s.

#46 The mainstream media has sold quantitative easing to the American public as an "economic stimulus program", but the truth is that the percentage of Americans that have a job has actually gone down since quantitative easing first began.

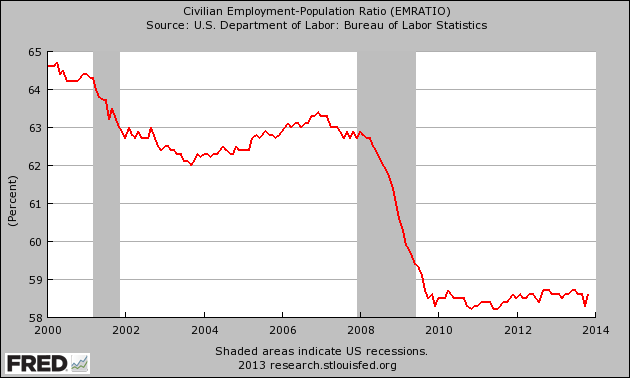

#47 The Federal Reserve is supposed to be able to guide the nation toward "full employment", but the reality of the matter is that an all-time record 102 million working age Americans do not have a job right now. That number has risen by about 27 million since the year 2000.

#48 For years, the projections of economic growth by the Federal Reserve have consistently overstated the strength of the U.S. economy. But every single time, the mainstream media continues to report that these numbers are "reliable" even though all they actually represent is wishful thinking.

#49 The Federal Reserve system fuels the growth of government, and the growth of government fuels the growth of the Federal Reserve system. Since 1970, federal spending has grown nearly 12 times as rapidly as median household income has.

#50 The Federal Reserve is supposed to look out for the health of all U.S. banks, but the truth is that they only seem to be concerned about the big ones. In 1985, there were more than 18,000 banks in the United States. Today, there are only 6,891 left.

#51 The six largest banks in the United States (JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, Goldman Sachs and Morgan Stanley) have collectively gotten 37 percent larger over the past five years.

#52 The U.S. banking system has 14.4 trillion dollars in total assets. The six largest banks now account for 67 percent of those assets and all of the other banks account for only 33 percent of those assets.

#53 The five largest banks now account for 42 percent of all loans in the United States.

#54 We were told that the purpose of quantitative easing is to help "stimulate the economy", but today the Federal Reserve is actually paying the big banks not to lend out 1.8 trillion dollars in "excess reserves" that they have parked at the Fed.

#55 The Federal Reserve has allowed an absolutely gigantic derivatives bubble to inflate which could destroy our financial system at any moment. Right now, four of the "too big to fail" banks each have total exposure to derivatives that is well in excess of 40 trillion dollars.

#56 The total exposure that Goldman Sachs has to derivatives contracts is more than 381 times greater than their total assets.

#57 Federal Reserve Chairman Ben Bernanke has a track record of failure that would make the Chicago Cubs look good.

#58 The secret November 1910 gathering at Jekyll Island, Georgia during which the plan for the Federal Reserve was hatched was attended by U.S. Senator Nelson W. Aldrich, Assistant Secretary of the Treasury Department A.P. Andrews and a whole host of representatives from the upper crust of the Wall Street banking establishment.

#59 The Federal Reserve was created by the big Wall Street banks and for the benefit of the big Wall Street banks.

#60 In 1913, Congress was promised that if the Federal Reserve Act was passed that it would eliminate the business cycle.

#61 There has never been a true comprehensive audit of the Federal Reserve since it was created back in 1913.

#62 The Federal Reserve system has been described as "the biggest Ponzi scheme in the history of the world".

#63 The following comes directly from the Fed's official mission statement: "To provide the nation with a safer, more flexible, and more stable monetary and financial system." Without a doubt, the Federal Reserve has failed in those tasks dramatically.

#64 The Fed decides what the target rate of inflation should be, what the target rate of unemployment should be and what the size of the money supply is going to be. This is quite similar to the "central planning" that goes on in communist nations, but very few people in our government seem upset by this.

#65 A couple of years ago, Federal Reserve officials walked into one bank in Oklahoma and demanded that they take down all the Bible verses and all the Christmas buttons that the bank had been displaying.

#66 The Federal Reserve has taken some other very frightening steps in recent years. For example, back in 2011 the Federal Reserve announced plans to identify "key bloggers" and to monitor "billions of conversations" about the Fed on Facebook, Twitter, forums and blogs. Someone at the Fed will almost certainly end up reading this article.

#67 Thanks to this endless debt spiral that we are trapped in, a massive amount of money is transferred out of our pockets and into the pockets of the ultra-wealthy each year. Incredibly, the U.S. government spent more than 415 billion dollars just on interest on the national debt in 2013.

#68 In September, the average rate of interest on the government’s marketable debt was 1.981 percent. In January 2000, the average rate of interest on the government’s marketable debt was 6.620 percent. If we got back to that level today, we would be paying more than a trillion dollars a year just in interest on the national debt and it would collapse our entire financial system.

#69 The American people are being killed by compound interest but most of them don't even understand what it is. Albert Einstein once made the following statement about compound interest...

#73 The following is what Thomas Edison once had to say about our absolutely insane debt-based financial system...

#75 Thomas Jefferson once stated that if he could add just one more amendment to the U.S. Constitution it would be a ban on all government borrowing....

#77 When the Federal Reserve was first established, the U.S. national debt was sitting at about 2.9 billion dollars. On average, we have been adding more than that to the national debt every single day since Obama has been in the White House.

#78 We are on pace to accumulate more new debt under the 8 years of the Obama administration than we did under all of the other presidents in all of U.S. history combined.

#79 If all of the new debt that has been accumulated since John Boehner became Speaker of the House had been given directly to the American people instead, every household in America would have been able to buy a new truck.

#80 Between 2008 and 2012, U.S. government debt grew by 60.7 percent, but U.S. GDP only grew by a total of about 8.5 percent during that entire time period.

#81 Since 2007, the U.S. debt to GDP ratio has increased from 66.6 percent to 101.6 percent.

#82 According to the U.S. Treasury, foreigners hold approximately 5.6 trillion dollars of our debt.

#83 The amount of U.S. government debt held by foreigners is about 5 times larger than it was just a decade ago.

#84 As I have written about previously, if the U.S. national debt was reduced to a stack of one dollar bills it would circle the earth at the equator 45 times.

#85 If Bill Gates gave every single penny of his entire fortune to the U.S. government, it would only cover the U.S. budget deficit for 15 days.

#86 Sometimes we forget just how much money a trillion dollars is. If you were alive when Jesus Christ was born and you spent one million dollars every single day since that point, you still would not have spent one trillion dollars by now.

#87 If right this moment you went out and started spending one dollar every single second, it would take you more than 31,000 years to spend one trillion dollars.

#88 In addition to all of our debt, the U.S. government has also accumulated more than 200 trillion dollars in unfunded liabilities. So where in the world will all of that money come from?

#89 The greatest damage that quantitative easing has been causing to our economy is the fact that it is destroying worldwide faith in the U.S. dollar and in U.S. debt. If the rest of the world stops using our dollars and stops buying our debt, we are going to be in a massive amount of trouble.

#90 Over the past several years, the Federal Reserve has been monetizing a staggering amount of U.S. government debt even though Ben Bernanke once promised that he would never do this.

#91 China recently announced that they are going to quit stockpiling more U.S. dollars. If the Federal Reserve was not recklessly printing money, this would probably not have happened.

#92 Most Americans have no idea that one of our most famous presidents was absolutely obsessed with getting rid of central banking in the United States. The following is a February 1834 quote by President Andrew Jackson about the evils of central banking....

#94 The capstone of the global central banking system is an organization known as the Bank for International Settlements. The following is how I described this organization in a previous article...

#96 Debt is a form of social control, and the global elite use all of this debt to dominate all the rest of us. 40 years ago, the total amount of debt in our system (all government debt, all business debt, all consumer debt, etc.) was sitting at about 2 trillion dollars. Today, the grand total exceeds 56 trillion dollars.

#97 Unless something dramatic is done, our children and our grandchildren will be debt slaves for their entire lives as they service our debts and pay for our mistakes.

#98 Now that you know this information, you are responsible for doing something about it.

#99 Congress has the power to shut down the Federal Reserve any time that they would like. But right now most of our politicians fully endorse the current system, and nothing is ever going to happen until the American people start demanding change.

#100 The design of the Federal Reserve system was flawed from the very beginning. If something is not done very rapidly, it is inevitable that our entire financial system is going to suffer an absolutely nightmarish collapse.

The truth is that we do not have to have a Federal Reserve. The greatest period of economic growth in U.S. history was when we did not have a central bank. If we are ever going to turn this nation around economically, we are going to have to get rid of this debt-based financial system that is centered around the Federal Reserve. On the path that we are on now, there is no hope. Please share this article with as many people as you can. It is imperative that we try to wake the American people up while we still have time.

#1 We like to think that we have a government "of the people, by the people, for the people", but the truth is that an unelected, unaccountable group of central planners has far more power over our economy than anyone else in our society does.

#2 The Federal Reserve is actually "independent" of the government. In fact, the Federal Reserve has argued vehemently in federal court that it is "not an agency" of the federal government and therefore not subject to the Freedom of Information Act.

#3 The Federal Reserve openly admits that the 12 regional Federal Reserve banks are organized "much like private corporations".

#4 The regional Federal Reserve banks issue shares of stock to the "member banks" that own them.

#5 100% of the shareholders of the Federal Reserve are private banks. The U.S. government owns zero shares.

#6 The Federal Reserve is not an agency of the federal government, but it has been given power to regulate our banks and financial institutions. This should not be happening.

#7 According to Article I, Section 8 of the U.S. Constitution, the U.S. Congress is the one that is supposed to have the authority to "coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures". So why is the Federal Reserve doing it?

#8 If you look at a "U.S. dollar", it actually says "Federal Reserve note" at the top. In the financial world, a "note" is an instrument of debt.

#9 In 1963, President John F. Kennedy issued Executive Order 11110 which authorized the U.S. Treasury to issue "United States notes" which were created by the U.S. government directly and not by the Federal Reserve. He was assassinated shortly thereafter.

#10 Many of the debt-free United States notes issued under President Kennedy are still in circulation today.

#11 The Federal Reserve determines what levels some of the most important interest rates in our system are going to be set at. In a free market system, the free market would determine those interest rates.

#12 The Federal Reserve has become so powerful that it is now known as "the fourth branch of government".

#13 The greatest period of economic growth in U.S. history was when there was no central bank.

#14 The Federal Reserve was designed to be a perpetual debt machine. The bankers that designed it intended to trap the U.S. government in a perpetual debt spiral from which it could never possibly escape. Since the Federal Reserve was established 100 years ago, the U.S. national debt has gotten more than 5000 times larger.

#15 A permanent federal income tax was established the exact same year that the Federal Reserve was created. This was not a coincidence. In order to pay for all of the government debt that the Federal Reserve would create, a federal income tax was necessary. The whole idea was to transfer wealth from our pockets to the federal government and from the federal government to the bankers.

#16 The period prior to 1913 (when there was no income tax) was the greatest period of economic growth in U.S. history.

#17 Today, the U.S. tax code is about 13 miles long.

#18 From the time that the Federal Reserve was created until now, the U.S. dollar has lost 98 percent of its value.

#19 From the time that President Nixon took us off the gold standard until now, the U.S. dollar has lost 83 percent of its value.

#20 During the 100 years before the Federal Reserve was created, the U.S. economy rarely had any problems with inflation. But since the Federal Reserve was established, the U.S. economy has experienced constant and never ending inflation.

#21 In the century before the Federal Reserve was created, the average annual rate of inflation was about half a percent. In the century since the Federal Reserve was created, the average annual rate of inflation has been about 3.5 percent.

#22 The Federal Reserve has stripped the middle class of trillions of dollars of wealth through the hidden tax of inflation.

#23 The size of M1 has nearly doubled since 2008 thanks to the reckless money printing that the Federal Reserve has been doing.

{kind=link}

#24 The Federal Reserve has been starting to behave like the Weimar Republic, and we all remember how that ended.

#25 The Federal Reserve has been consistently lying to us about the level of inflation in our economy. If the inflation rate was still calculated the same way that it was back when Jimmy Carter was president, the official rate of inflation would be somewhere between 8 and 10 percent today.

#26 Since the Federal Reserve was created, there have been 18 distinct recessions or depressions: 1918, 1920, 1923, 1926, 1929, 1937, 1945, 1949, 1953, 1958, 1960, 1969, 1973, 1980, 1981, 1990, 2001, 2008.

#27 Within 20 years of the creation of the Federal Reserve, the U.S. economy was plunged into the Great Depression.

#28 The Federal Reserve created the conditions that caused the stock market crash of 1929, and even Ben Bernanke admits that the response by the Fed to that crisis made the Great Depression even worse than it should have been.

#29 The "easy money" policies of former Fed Chairman Alan Greenspan set the stage for the great financial crisis of 2008.

#30 Without the Federal Reserve, the "subprime mortgage meltdown" would probably never have happened.

#31 If you can believe it, there have been 10 different economic recessions since 1950. The Federal Reserve created the "dotcom bubble", the Federal Reserve created the "housing bubble" and now it has created the largest bond bubble in the history of the planet.

#32 According to an official government report, the Federal Reserve made 16.1 trillion dollars in secret loans to the big banks during the last financial crisis. The following is a list of loan recipients that was taken directly from page 131 of the report...

Citigroup - $2.513 trillion

Morgan Stanley - $2.041 trillion

Merrill Lynch - $1.949 trillion

Bank of America - $1.344 trillion

Barclays PLC - $868 billion

Bear Sterns - $853 billion

Goldman Sachs - $814 billion

Royal Bank of Scotland - $541 billion

JP Morgan Chase - $391 billion

Deutsche Bank - $354 billion

UBS - $287 billion

Credit Suisse - $262 billion

Lehman Brothers - $183 billion

Bank of Scotland - $181 billion

BNP Paribas - $175 billion

Wells Fargo - $159 billion

Dexia - $159 billion

Wachovia - $142 billion

Dresdner Bank - $135 billion

Societe Generale - $124 billion

"All Other Borrowers" - $2.639 trillion

#33 The Federal Reserve also paid those big banks $659.4 million in "fees" to help "administer" those secret loans.

#34 During the last financial crisis, big European banks were allowed to borrow an "unlimited" amount of money from the Federal Reserve at ultra-low interest rates.

#35 The "easy money" policies of Federal Reserve Chairman Ben Bernanke have created the largest financial bubble this nation has ever seen, and this has set the stage for the great financial crisis that we are rapidly approaching.

#36 Since late 2008, the size of the Federal Reserve balance sheet has grown from less than a trillion dollars to more than 4 trillion dollars. This is complete and utter insanity.

#37 During the quantitative easing era, the value of the financial securities that the Fed has accumulated is greater than the total amount of publicly held debt that the U.S. government accumulated from the presidency of George Washington through the end of the presidency of Bill Clinton.

#38 Overall, the Federal Reserve now holds more than 32 percent of all 10 year equivalents, and that percentage is rising by about 0.3 percent each week.

#39 Quantitative easing creates financial bubbles, and when quantitative easing ends those bubbles tend to deflate rapidly.

#40 Most of the new money created by quantitative easing has ended up in the hands of the very wealthy.

#41 According to a prominent Federal Reserve insider, quantitative easing has been one giant "subsidy" for Wall Street banks.

#42 As one CNBC article recently stated, we are seeing absolutely rampant inflation in "stocks and bonds and art and Ferraris".

#43 Donald Trump once made the following statement about quantitative easing: "People like me will benefit from this."

#44 Most people have never heard about this, but a very interesting study conducted for the Bank of England shows that quantitative easing actually increases the gap between the wealthy and the poor.

#45 The gap between the top one percent and the rest of the country is now the greatest that it has been since the 1920s.

#46 The mainstream media has sold quantitative easing to the American public as an "economic stimulus program", but the truth is that the percentage of Americans that have a job has actually gone down since quantitative easing first began.

{kind=link}

#47 The Federal Reserve is supposed to be able to guide the nation toward "full employment", but the reality of the matter is that an all-time record 102 million working age Americans do not have a job right now. That number has risen by about 27 million since the year 2000.

#48 For years, the projections of economic growth by the Federal Reserve have consistently overstated the strength of the U.S. economy. But every single time, the mainstream media continues to report that these numbers are "reliable" even though all they actually represent is wishful thinking.

#49 The Federal Reserve system fuels the growth of government, and the growth of government fuels the growth of the Federal Reserve system. Since 1970, federal spending has grown nearly 12 times as rapidly as median household income has.

#50 The Federal Reserve is supposed to look out for the health of all U.S. banks, but the truth is that they only seem to be concerned about the big ones. In 1985, there were more than 18,000 banks in the United States. Today, there are only 6,891 left.

#51 The six largest banks in the United States (JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, Goldman Sachs and Morgan Stanley) have collectively gotten 37 percent larger over the past five years.

#52 The U.S. banking system has 14.4 trillion dollars in total assets. The six largest banks now account for 67 percent of those assets and all of the other banks account for only 33 percent of those assets.

#53 The five largest banks now account for 42 percent of all loans in the United States.

#54 We were told that the purpose of quantitative easing is to help "stimulate the economy", but today the Federal Reserve is actually paying the big banks not to lend out 1.8 trillion dollars in "excess reserves" that they have parked at the Fed.

#55 The Federal Reserve has allowed an absolutely gigantic derivatives bubble to inflate which could destroy our financial system at any moment. Right now, four of the "too big to fail" banks each have total exposure to derivatives that is well in excess of 40 trillion dollars.

#56 The total exposure that Goldman Sachs has to derivatives contracts is more than 381 times greater than their total assets.

#57 Federal Reserve Chairman Ben Bernanke has a track record of failure that would make the Chicago Cubs look good.

#58 The secret November 1910 gathering at Jekyll Island, Georgia during which the plan for the Federal Reserve was hatched was attended by U.S. Senator Nelson W. Aldrich, Assistant Secretary of the Treasury Department A.P. Andrews and a whole host of representatives from the upper crust of the Wall Street banking establishment.

#59 The Federal Reserve was created by the big Wall Street banks and for the benefit of the big Wall Street banks.

#60 In 1913, Congress was promised that if the Federal Reserve Act was passed that it would eliminate the business cycle.

#61 There has never been a true comprehensive audit of the Federal Reserve since it was created back in 1913.

#62 The Federal Reserve system has been described as "the biggest Ponzi scheme in the history of the world".

#63 The following comes directly from the Fed's official mission statement: "To provide the nation with a safer, more flexible, and more stable monetary and financial system." Without a doubt, the Federal Reserve has failed in those tasks dramatically.

#64 The Fed decides what the target rate of inflation should be, what the target rate of unemployment should be and what the size of the money supply is going to be. This is quite similar to the "central planning" that goes on in communist nations, but very few people in our government seem upset by this.

#65 A couple of years ago, Federal Reserve officials walked into one bank in Oklahoma and demanded that they take down all the Bible verses and all the Christmas buttons that the bank had been displaying.

#66 The Federal Reserve has taken some other very frightening steps in recent years. For example, back in 2011 the Federal Reserve announced plans to identify "key bloggers" and to monitor "billions of conversations" about the Fed on Facebook, Twitter, forums and blogs. Someone at the Fed will almost certainly end up reading this article.

#67 Thanks to this endless debt spiral that we are trapped in, a massive amount of money is transferred out of our pockets and into the pockets of the ultra-wealthy each year. Incredibly, the U.S. government spent more than 415 billion dollars just on interest on the national debt in 2013.

#68 In September, the average rate of interest on the government’s marketable debt was 1.981 percent. In January 2000, the average rate of interest on the government’s marketable debt was 6.620 percent. If we got back to that level today, we would be paying more than a trillion dollars a year just in interest on the national debt and it would collapse our entire financial system.

#69 The American people are being killed by compound interest but most of them don't even understand what it is. Albert Einstein once made the following statement about compound interest...