The written responses to Warren’s queries came back last week (see the full text at the end of this post). Warren criticized Treasury’s failure to do its own homework on the whether large banks can borrow money more cheaply by virtue of being perceived as being too big to fail. As Bloomberg noted:

U.S. Senator Elizabeth Warren criticized the Treasury Department for not conducting a formal study to determine if some banks receive a funding subsidy for being perceived to be too big to fail.

“The best way to make an objective determination of whether too-big-to-fail continues to exist over time is by measuring the subsidy, and Treasury should develop its own metrics for doing so through the Office of Financial Research,” Warren, a Massachusetts Democrat, said today in an e-mailed statement.This question matters not just because it’s precisely the sort of thing the Office of Financial Research ought to be doing, but also because Treasury has the leading role on the Financial Stability Oversight Council. But peculiarly, Treasury takes the position that it can rely on third-party research. Given the banks’ role in supporting various think tanks and funding finance programs at business schools, one would have to assume that Treasury knows full well that a lot of that “research” is lobbying using charts and data as decoration. By contrast, in the UK, the Bank of England not only prepares an impressively detailed Financial Stability Report twice a year, but when Andrew Haldane was its executive director of financial stability, he gave detailed estimates of the funding cost advantage of the big UK and global banks. So if England thinks preparing this sort of analysis is part of the “financial stability overseer” job description, it’s telling that Treasury has chosen to shirk it.

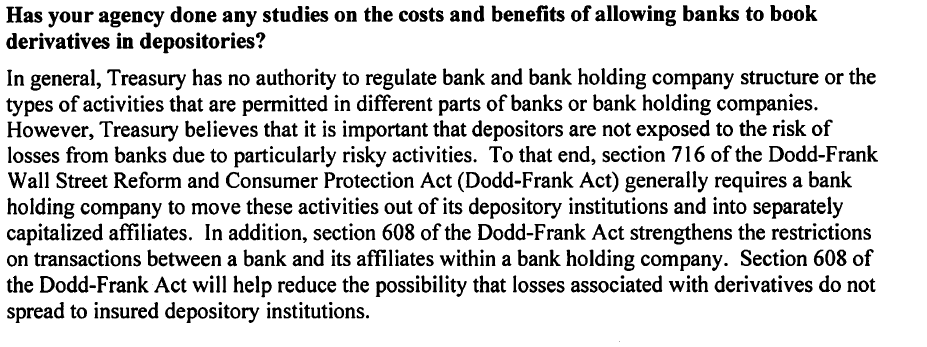

But if I were Warren, I’d be at least as unhappy about Treasury’s misdirections. For instance, get a load of this (click to enlarge):

Translation: We’re sympathetic, but not our job.

But that’s not the whole story.

There was a big brouhaha in 2011 when Bank of America moved $75 trillion (yes, trillion) of derivatives from its holding company to its retail bank to avoid having to post $3.3 billion of extra collateral after a downgrade. The FDIC was opposed to the move. The Fed supported it. And the Treasury? Nowhere to be found, at least from what I can recall at the time plus some searching this evening.

Yet the Treasury had a dog in this fight, both via its role on FSOC and as potential funder of Bank of America. As Jonathan Weil pointed out in 2011:

Dodd-Frank lets the FDIC borrow money from the Treasury to finance a seized company’s operations for as long as five years. While the law says the FDIC is supposed to tap the banking industry to pay for any eventual losses, it’s hard to imagine the agency could ever charge enough to cover the costs from a failure at a company with $2.2 trillion of assets, or any other giant financial institution, for that matter. Plus, there’s always the chance Congress will change the law again.But at this juncture (before the various get out of jail free cards known as mortgage settlements had come to pass), Treasury’s priority was to help shore up the wobbly Charlotte bank. Remaining silent in the Fed/FDIC argument over the Bank of America derivatives assured the Fed as more senior regulator would win.

So the Treasury has a history on this topic, and it’s the opposite of the posturing about being concerned about depositor risk exposures.* And notice how talking about depositor risk sidesteps the big issue about booking derivatives in depositaries: the whole point is, as the Bank of America example shows, to lower funding costs, meaning to have deposit insurance and the taxpayer backstop subsidize the derivatives casino. Warren’s next question hones in on that issue, as to whether Treasury has looked into what OTC derivatives are really used for and how much of it is socially productive. Again, Treasury answers a different question and makes motherhood and apple pie statements about how Dodd Frank reduces opacity in the OTC derivatives markets.

Similarly, in response to question 4 on borrowing costs, Treasury says in passing:

The emergency resolution authority created under Title II [of Dodd Frank] explicitly forbids any bailout by taxpayers.That’s a minority view. First, William Dudley of the New York Fed said late last year that Title II resolutions won’t work with the firms everyone is most worried about, globe-sprawling behemoths. As we wrote then:

The New York Fed’s William Dudley gave a surprisingly candid, meaning not positive, assessment of the state of the Too Big to Fail problem in a speech yesterday at the Clearing House’s Second Annual Business Meeting and Conference. From the text of his speech(emphasis ours)….:

In my view, this initial exercise has confirmed that we are a long way from the desired situation in which large complex firms could be allowed to go bankrupt without major disruptions to the financial system and large costs to society. Significant changes in structure and organization will ultimately be required for this to be achieved. However, the “living will” exercise is an iterative process, and we have only taken the first step in a long journey.

The second way to potentially minimize the negative externalities from a firm’s failure would be to avoid a bankruptcy proceeding altogether and instead resolve the firm under the Dodd-Frank Act’s Title II orderly liquidation 7 authority.8

The “single point of entry” model has much promise, but much remains to be done before it could be implemented with confidence for a globally active firm. Title II authority is U.S. law. Subsidiaries and affiliates chartered in other countries could be wound down under the bankruptcy laws of those countries, if authorities there did not have full confidence that local interests would be protected. Certain Title II measures including the one-day stay provision with respect to OTC derivatives and other qualified financial contracts may not apply through the force of law outside the United States, making orderly resolution difficult.Second, and more important, Spencer Bachus, Chairman of the House Financial Services Committee, pointed out in a paper published a month before the Dudley speech that despite the claims of Dodd Frank fans that it barred bailouts, it leaves plenty of room for rescues:

Among other things, the “resolution authority” gives the FDIC the power to lend to a fail- ing firm; purchase its assets; guarantee its obligations; and — most important — pay off its creditors. The “resolution authority” also gives the FDIC the authority to borrow money from the Treasury. Lots of it. How much? The FDIC can borrow up to 10% of the book value of the failed firm’s total consolidated assets in the 30 days immediately following its appointment as receiver. After those 30 days, the FDIC can borrow up to 90% of the fair value of the failed firm’s total consolidated assets.Tellingly, the Bloomberg story on the Warren letter has no less than Jacob Lew undercutting its claims about Dodd Frank resolutions:

Treasury Secretary Jacob J. Lew in July said that if too big to fail is not solved by the end of this year “we’re going to have to look at other options.” He didn’t elaborate on what alternatives President Barack Obama’s administration might consider.So Treasury can’t even keep its stories straight. Let’s hope Warren is keeping score and has a bit of sport the next time its officials make an appearance before the Senate Banking Committee. If she can’t get them to change behavior, she can at least make clear that no one is buying their excuses.

Source

0 comments:

Post a Comment