Frontline has created a video called The Untouchables (January 22, 2013) that "investigates why Wall Street's leaders have escaped prosecution for any fraud related to the sale of bad mortgages."

This video explores why no criminal liability for fraud was brought against the banks or mortgage originators. In short, the banks were not investigated for fraud so, of course, no fraud was found.

Names are named such as Lanny Breuer who recently resigned from the Department of Justice after being interviewed by Frontline and Angelo Mozilo, former Countrywide CEO. All the usual suspects are there: Robert Rubin, Dick Fuld, etc.

Senator Ted Kaufman was a man of honor fighting this corruption as was Jeff Connaughton, Carl Levin and other committee heads that investigated those responsible for the financial crisis. Then there were those who could have made a difference and chose not to like Eric Schneiderman.

Certainly the President's desire to look forward and not backward was the main incentive not to investigate or criminally prosecute the executives of the banks, including Lloyd Blankfein of Goldman Sachs. For the past few years he has been "breathing a sigh of relief."

See the Frontline video and other videos and articles on the financial meltdown here

See William K. Black's detailed analysis of Goldman Sachs destruction of the economy here

Source

Federal Reserve Money Printing Is The Real Reason Why The Stock Market Is Soaring

You can thank the reckless money printing that the Federal Reserve has been doing for the incredible bull market that we have seen in recent months. When the Federal Reserve does more "quantitative easing", it is the financial markets that benefit the most. The Dow and the S&P 500 have both hit levels not seen since 2007 this month, and many analysts are projecting that 2013 will be a banner year for stocks. But is a rising stock market really a sign that the overall economy is rapidly improving as many are suggesting? Of course not. Just because the Federal Reserve has inflated another false stock market bubble with a bunch of funny money does not mean that the U.S. economy is in great shape. In fact, the truth is that things just keep getting worse for average Americans. The percentage of working age Americans with a job has fallen from 60.6% to 58.6% while Barack Obama has been president, 40 percent of all American workers are making $20,000 a year or less, median household income has declined for four years in a row, and poverty in the United States is absolutely exploding. So quantitative easing has definitely not made things better for the middle class. But all of the money printing that the Fed has been doing has worked out wonderfully for Wall Street. Profits are soaring at Goldman Sachs and luxury estates in the Hamptons are selling briskly. Unfortunately, this is how things work in America these days. Our "leaders" seem far more concerned with the welfare of Wall Street than they do about the welfare of the American people. When things get rocky, their first priority always seems to be to do whatever it takes to pump up the financial markets.

When QE3 was announced, it was heralded as the grand solution to all of our economic problems. But the truth is that those running things knew exactly what it would do. Quantitative easing always pumps up the financial markets, and that overwhelmingly benefits those that are wealthy. In fact, a while back a CNBC article discussed a very interesting study from the Bank of England which showed a clear correlation between quantitative easing and rising stock prices...

Of course not.

And who benefits from this?

The wealthy do. In fact, 82 percent of all individually held stocks are owned by the wealthiest 5 percent of all Americans.

Unfortunately, all of this reckless money printing has a very negative impact on all the rest of us. When the Fed floods the financial system with money, that causes inflation. That means that the cost of living has gone up even though your paycheck may not have.

If you go to the supermarket frequently, you know exactly what I am talking about. The new "sale prices" are what the old "regular prices" used to be. They keep shrinking many of the package sizes in order to try to hide the inflation, but I don't think many people are fooled. Our food dollars are not stretching nearly as far as they used to, and we can blame the Federal Reserve for that.

For much more on rising prices in America, please see this article: "Somebody Should Start The ‘Stuff Costs Too Much’ Party".

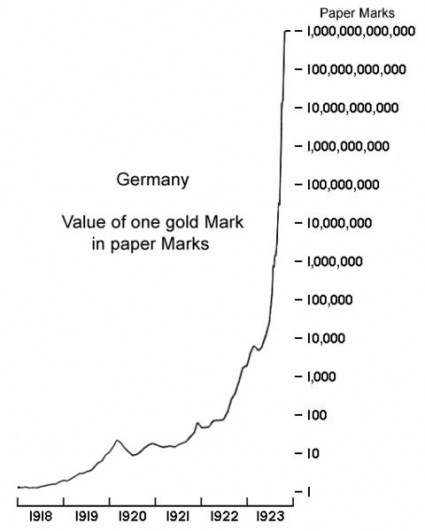

Sadly, this is what the Federal Reserve does. The system was designed to create inflation. Before the Federal Reserve came into existence, the United States never had an ongoing problem with inflation. But since the Fed was created, the United States has endured constant inflation. In fact, we have come to accept it as "normal". Just check out the amazing chart in the video posted below...

The chart in that video kind of reminds me of a chart that I shared in a previous article...

Not that I expect the United States to enter a period of hyperinflation in the near future.

Not that I expect the United States to enter a period of hyperinflation in the near future.

Actually, despite all of the reckless money printing that the Fed has been doing, I expect that at some point we are going to see another wave of panic hit the financial markets like we saw back in 2008. The false stock market bubble will burst, major banks will fail and the financial system will implode. It could unfold something like this...

1 - A derivatives panic hits the "too big to fail" banks.

2 - Financial markets all over the globe crash.

3 - The credit markets freeze up.

4 - Economic activity in the United States starts to grind to a halt.

5 - Unemployment rises above 20 percent and mortgage defaults soar to unprecedented levels.

6 - Tax revenues fall dramatically and austerity measures are implemented by the federal government, state governments and local governments.

7 - The rest of the globe rapidly loses confidence in the U.S. financial system and begins to dump U.S. debt and U.S. dollars.

I write about derivatives a lot, because they are one of the greatest threats that the global financial system is facing. In fact, right now a derivatives scandal is threatening to take down the oldest bank in the world...

In response to the coming financial crisis, I believe that our "leaders" will eventually resort to money printing unlike anything we have ever seen before in a desperate attempt to resuscitate the system. When that happens, I believe that we will see the kind of rampant inflation that so many people have been warning about.

So what do you think about all of this?

Do you believe that Federal Reserve money printing is the real reason why the stock market is soaring?

Source

When QE3 was announced, it was heralded as the grand solution to all of our economic problems. But the truth is that those running things knew exactly what it would do. Quantitative easing always pumps up the financial markets, and that overwhelmingly benefits those that are wealthy. In fact, a while back a CNBC article discussed a very interesting study from the Bank of England which showed a clear correlation between quantitative easing and rising stock prices...

It said that the Bank of England’s policies of quantitative easing – similar to the Fed’s – had benefited mainly the wealthy.

Specifically, it said that its QE program had boosted the value of stocks and bonds by 26 percent, or about $970 billion. It said that about 40 percent of those gains went to the richest 5 percent of British households.

Many said the BOE's easing added to social anger and unrest. Dhaval Joshi, of BCA Research wrote that “QE cash ends up overwhelmingly in profits, thereby exacerbating already extreme income inequality and the consequent social tensions that arise from it."So should we be surprised that stocks are now the highest that they have been in more than 5 years?

Of course not.

And who benefits from this?

The wealthy do. In fact, 82 percent of all individually held stocks are owned by the wealthiest 5 percent of all Americans.

Unfortunately, all of this reckless money printing has a very negative impact on all the rest of us. When the Fed floods the financial system with money, that causes inflation. That means that the cost of living has gone up even though your paycheck may not have.

If you go to the supermarket frequently, you know exactly what I am talking about. The new "sale prices" are what the old "regular prices" used to be. They keep shrinking many of the package sizes in order to try to hide the inflation, but I don't think many people are fooled. Our food dollars are not stretching nearly as far as they used to, and we can blame the Federal Reserve for that.

For much more on rising prices in America, please see this article: "Somebody Should Start The ‘Stuff Costs Too Much’ Party".

Sadly, this is what the Federal Reserve does. The system was designed to create inflation. Before the Federal Reserve came into existence, the United States never had an ongoing problem with inflation. But since the Fed was created, the United States has endured constant inflation. In fact, we have come to accept it as "normal". Just check out the amazing chart in the video posted below...

The chart in that video kind of reminds me of a chart that I shared in a previous article...

Actually, despite all of the reckless money printing that the Fed has been doing, I expect that at some point we are going to see another wave of panic hit the financial markets like we saw back in 2008. The false stock market bubble will burst, major banks will fail and the financial system will implode. It could unfold something like this...

1 - A derivatives panic hits the "too big to fail" banks.

2 - Financial markets all over the globe crash.

3 - The credit markets freeze up.

4 - Economic activity in the United States starts to grind to a halt.

5 - Unemployment rises above 20 percent and mortgage defaults soar to unprecedented levels.

6 - Tax revenues fall dramatically and austerity measures are implemented by the federal government, state governments and local governments.

7 - The rest of the globe rapidly loses confidence in the U.S. financial system and begins to dump U.S. debt and U.S. dollars.

I write about derivatives a lot, because they are one of the greatest threats that the global financial system is facing. In fact, right now a derivatives scandal is threatening to take down the oldest bank in the world...

Banca Monte dei Paschi di Siena, the world’s oldest bank, was making loans when Michelangelo and Leonardo da Vinci were young men and before Columbus sailed to the New World. The bank survived the Italian War, which saw Siena’s surrender to Spain in 1555, the Napoleonic campaign, the Second World War and assorted bouts of plague and poverty.So when you hear the word "derivatives" in the news, pay close attention. The bankers have turned our financial system into a giant casino, and at some point the entire house of cards is going to come crashing down.

But MPS may not survive the twin threats of a gruesomely expensive takeover gone bad and a derivatives scandal that may result in legal action against the bank’s former executives. After five centuries of independence, MPS may have to be nationalized as its losses soar and its value sinks.

In response to the coming financial crisis, I believe that our "leaders" will eventually resort to money printing unlike anything we have ever seen before in a desperate attempt to resuscitate the system. When that happens, I believe that we will see the kind of rampant inflation that so many people have been warning about.

So what do you think about all of this?

Do you believe that Federal Reserve money printing is the real reason why the stock market is soaring?

Source

BoE's Haldane: "Too Big To Fail Is Far From Gone"

Have We Solved 'Too Big To Fail'?

No.

That is not my pessimistic verdict; it is the market’s. Prior to the crisis, the 29 largest global banks benefitted from just over one notch of uplift from the ratings agencies due to expectations of state support. Today, those same global leviathans benefit from around three notches of implied support. Expectations of state support have risen threefold since the crisis began.

This translates into a large implicit subsidy to the world’s biggest banks in the form of lower funding costs and higher profits. Prior to the crisis, this amounted to tens of billions of dollars each year. Today, it is hundreds of billions (Haldane 2012). In other words, if the market’s expectations are to be believed, the regulatory response to the crisis has not plugged the 'too-big-to-fail' sink.

On the face of it, that sounds perplexing. Rarely a day passes without a warning from the financial industry about overbearing regulation of, in particular, the world’s biggest banks. What is certainly true is that, in the light of the crisis, regulation to quell the too-big-to-fail problem has come thick and (at least in regulatory terms) fast. This reform effort falls into roughly three categories:

Another more radical option, mooted recently by a number of commentators and policymakers, would be to place size limits on banks, either in relation to the financial system as a whole or, more coherently, relative to GDP (Hoenig (2012), Tarullo (2012)). Proposals of this type typically face two sets of criticism.

The first, practical issue is how to calibrate an appropriate limit. Recent research on the link between and financial depth and growth provides a way into this question. This research has suggested that there is a threshold at which the private-credit-to-GDP ratio may begin to have a negative impact on GDP and, in particular, productivity growth (Arcand et al (2012), Cechetti and Kharroubi (2012)). By taking a view on this aggregate threshold, and on an appropriate degree of concentration within the financial system, an institution-specific threshold could be derived.

The second, empirical issue is whether size limits would erode the economies of scale and scope which might otherwise be associated with big banks. The empirical literature on these economies has, until recently, suggested they may be exhausted at relatively low balance sheet thresholds. But a number of recent papers have painted a more optimistic picture, with economies of scale found for banks with balance sheets in excess of $1 trillion (Wheelock and Wilson (2012), Feng and Serilitis (2009), Hughes and Mester (2011)).

Yet this evidence needs to be interpreted cautiously, not least because it fails to recognise the implicit subsidies associated with too-big-to-fail. These would tend to lower funding costs and boost measured valued-added for the big banks. In other words, the implicit subsidy would show up as economies of scale. Bank of England research has recently shown that, once those subsidies are accounted for, evidence of scale economies for banks with assets in excess of $100 billion tends to disappear (Davies and Tracey (2012)). Indeed, if anything, there may even be evidence of scale diseconomies, perhaps consistent with big banks being 'too big to manage'.

Too-big-to-fail is far from gone. It is even more important it is not forgotten. Further analytical work, weighing the costs and benefits of different structural reform proposals, would help keep memories fresh and policies on the right track.

Source

No.

That is not my pessimistic verdict; it is the market’s. Prior to the crisis, the 29 largest global banks benefitted from just over one notch of uplift from the ratings agencies due to expectations of state support. Today, those same global leviathans benefit from around three notches of implied support. Expectations of state support have risen threefold since the crisis began.

This translates into a large implicit subsidy to the world’s biggest banks in the form of lower funding costs and higher profits. Prior to the crisis, this amounted to tens of billions of dollars each year. Today, it is hundreds of billions (Haldane 2012). In other words, if the market’s expectations are to be believed, the regulatory response to the crisis has not plugged the 'too-big-to-fail' sink.

On the face of it, that sounds perplexing. Rarely a day passes without a warning from the financial industry about overbearing regulation of, in particular, the world’s biggest banks. What is certainly true is that, in the light of the crisis, regulation to quell the too-big-to-fail problem has come thick and (at least in regulatory terms) fast. This reform effort falls into roughly three categories:

(a) Systemic surcharges: of additional capital levied on the world’s largest banks according to their size and connectivity. This Pigouvian tax on systemic risk externalities is built on conceptually sound foundations (for example, Brunnermeier 2009). And, encouragingly, good economics has found its way into good public policy. Last year, the Financial Stability Board (FSB) agreed a sliding scale of systemic surcharges for the world’s largest banks. The highest surcharge was set at 2.5% of capital.If each of these initiatives is necessary but none is individually or collectively sufficient to tackle too-big-to-fail, what is to be done? One solution might lie in strengthening these proposals. For example, re-sizing the capital surcharge, perhaps in line with quantitative estimates of the 'optimal' capital ratio (Miles et al (2012), Admati et al (2011)), would be one option for bearing down further on systemic externalities.

Yet therein lies the problem. Based on my estimates (Haldane 2012), a charge levied at this rate would leave the majority of the systemic externalities associated with the world’s biggest banks untouched. The reduction in default probabilities associated with lowering leverage by a percentage point or two would not offset the higher system-wide loss-given-default associated with the world’s largest banks. The systemic tax is being levied at rates which are too low to meet Pigouvian ends.

(b) Resolution regimes: In principle, orderly resolution regimes for banks could lower the collateral costs of a big bank defaulting, thereby tackling at source these systemic externalities. And significant public policy progress has been made on this front, with the FSB publishing (and the G20 approving) some Key Attributes for Effective Resolution Regimes during the course of the past 18 months. A key component of these plans is the ability to impose losses on private creditors – so-called 'bail-in' – rather than have those losses borne by taxpayers.

As with systemic surcharges, the issue here is not to so much the bail-in principle, but its application in practice. Bail-in, whether of big banks, sovereigns or companies, faces an acute time-consistency problem. Policymakers face a trade-off between placing losses on a narrow set of tax-payers today (bail-in) or spreading that risk across a wider set of tax-payers today and tomorrow (bail-out).

A risk-averse, tax-smoothing government may tend towards the latter path – and historically has almost always done so, most notably in response to the present financial crisis. Next time may of course be different. But the market is sceptical. For example, in the US the Dodd-Frank Act on paper rules in future bail-in and rules out future bail-out. Yet market expectations of state support for US banks are higher today than before the crisis struck and are unchanged since Dodd-Frank became law. The time-consistency dilemma, at least in the eyes of markets, is as acute as ever.

(c) Structural reform: One way of lessening that dilemma may be to act on the scale and structure of banking directly. Several recent regulatory reform initiatives have sought to do just that, notably the “Volcker rule” in the US, the 'Vickers proposals' in the UK and, most recently, the 'Liikanen plans' in Europe. While different in detail, each of these proposals shares a common objective: a degree of separation or segregation between investment and commercial banking activities.

In principle, these ringfencing initiatives confer both ex-post (improved resolution) and ex-ante (improved risk management) benefits. Because they act on banking structure, they have a greater chance of proving time-consistent. While this is a clear step forward, those benefits are only as credible as the ringfence itself. The issue raised by some is whether, in practice, the ring-fence could prove permeable. Without care, today’s ring-fence could become tomorrow’s string vest.

Another more radical option, mooted recently by a number of commentators and policymakers, would be to place size limits on banks, either in relation to the financial system as a whole or, more coherently, relative to GDP (Hoenig (2012), Tarullo (2012)). Proposals of this type typically face two sets of criticism.

The first, practical issue is how to calibrate an appropriate limit. Recent research on the link between and financial depth and growth provides a way into this question. This research has suggested that there is a threshold at which the private-credit-to-GDP ratio may begin to have a negative impact on GDP and, in particular, productivity growth (Arcand et al (2012), Cechetti and Kharroubi (2012)). By taking a view on this aggregate threshold, and on an appropriate degree of concentration within the financial system, an institution-specific threshold could be derived.

The second, empirical issue is whether size limits would erode the economies of scale and scope which might otherwise be associated with big banks. The empirical literature on these economies has, until recently, suggested they may be exhausted at relatively low balance sheet thresholds. But a number of recent papers have painted a more optimistic picture, with economies of scale found for banks with balance sheets in excess of $1 trillion (Wheelock and Wilson (2012), Feng and Serilitis (2009), Hughes and Mester (2011)).

Yet this evidence needs to be interpreted cautiously, not least because it fails to recognise the implicit subsidies associated with too-big-to-fail. These would tend to lower funding costs and boost measured valued-added for the big banks. In other words, the implicit subsidy would show up as economies of scale. Bank of England research has recently shown that, once those subsidies are accounted for, evidence of scale economies for banks with assets in excess of $100 billion tends to disappear (Davies and Tracey (2012)). Indeed, if anything, there may even be evidence of scale diseconomies, perhaps consistent with big banks being 'too big to manage'.

Too-big-to-fail is far from gone. It is even more important it is not forgotten. Further analytical work, weighing the costs and benefits of different structural reform proposals, would help keep memories fresh and policies on the right track.

Source

Bill Black: Why the World Economic Forum and Goldman Sachs are Capitalism’s Worst Enemies

It is fitting that Goldman Sachs is the recipient of this year’s “Public Eye” designation, but it is even more fitting that it is being announced during the World Economic Forum (WEF) at Davos. Goldman Sachs exemplifies the travesty that WEF has created. It is not the worst of the worst. It is representative of the financial world of systemically dangerous institutions (SDIs) that are spreading crony capitalism through the West. The SDIs are the so-called “too big to fail (or prosecute)” banks.

The ability of the SDIs to commit fraud with impunity from the criminal laws is a defining element of crony capitalism. The impunity and implicit national subsidies to SDIs combine to make “free markets” an oxymoron. The SDIs’ economic power translates easily into dominant political power. Crony capitalism cripples markets and democracy.

The ability of the SDIs’ senior officers to commit massive frauds with impunity from the criminal laws makes “control fraud” a “sure thing.” Control fraud will make the largest banks’ senior officers exceptionally wealthy very quickly – but it will also cause severe harm to the public (and often the bank). Control fraud occurs when the persons who control a seemingly legitimate entity use it as a “weapon” to defraud. In finance, accounting is the “weapon of choice.” It is important to remember, however, that other forms of control fraud maim and kill hundreds of thousands and cause grave environmental damage. We must always remember the infant formula scandal in China where 300,000 infants were hospitalized with kidney stones due to consumer frauds that drove every honest manufacturer out of business.

Large, individual accounting control frauds cause greater financial losses than all other forms of property crime – combined. Accounting control frauds are weapons of mass financial destruction. Epidemics of accounting control fraud drove the national crises that produced the Great Recession. We have reliable information on this in the United States, the United Kingdom, Ireland, and Iceland. Spain has kept the facts about lending too opaque to determine reliably what caused their bubble to hyper-inflate, but the lending pattern is consistent with accounting control fraud. These accounting control fraud epidemics drove crises that caused a loss of over $20 trillion in wealth and cost roughly 20 million workers their jobs.

These epidemics of accounting control fraud were not random “black swan” events. Criminogenic environments produce such intense and perverse incentives that they generate epidemics of control fraud. Our financial policies have been so criminogenic for decades that we are suffering recurrent, intensifying financial crises. WEF is one of the important architects and engineers that have made our financial system so criminogenic. WEF’s dogmas and policies are so perverse that they drive financial crises, create crony capitalism, and make WEF’s leading products (the Global Competitiveness Index (GCI) and Global Risk Reports (GRR) epic embarrassments. The WEF is degrading the state of the world.

Criminogenic environments for Accounting Control Fraud

Fraud Deniers

In 2012, in response to endemic, elite financial frauds, the WEF declared the following without citation or reasoning in its 2012 report on “Rethinking Financial Innovation.”

The leading “law and economics” text on corporate law has taught a generation of American lawyers that “a rule against fraud is not an essential or … an important ingredient of securities markets” (Easterbrook & Fischel 1991).

WEF’s founding ideology is “stakeholder” theory – the philosophical belief that a corporation should serve the interests of its stakeholders. The stakeholders include stockholders, creditors, and workers. Variants of control fraud target each of these stakeholders. Control frauds, therefore, are the kryptonite to stakeholder theory. Control frauds drive stakes through their stakeholders. WEF’s solution is to assume away reality. WEF ignores the findings about control fraud made by modern criminology, effective regulators and prosecutors, and top economists and to embrace Greenspan’s dogma even after Greenspan has abandoned it.

I cite information below on the dominant role of fraud during the savings and loan debacle. The role of accounting control fraud in the Enron-era is not in dispute. My FCIC testimony details the extraordinary levels of accounting control fraud driving the U.S. crisis. (I have other papers discussing the decisive role of accounting control fraud in Ireland and Iceland.) The briefest version is that by 2006, roughly 40% of mortgage loans made that year were “liar’s” loans. The incidence of fraud in liar’s loans is 90%. Lenders put the lies in liar’s loans.

The figure for liar’s loans was even higher in the UK. On January 25, 2012, Martin Wheatley delivered a speech to the British Bankers’ Association entitled “My Vision for the FCA.”

The Three “De’s” and the First Virgin Crisis

George Akerlof was made the Nobel Laureate in Economics in 2001. He co-authored a famous article in 1993 about accounting control fraud (“Looting: the Economic Underworld of Bankruptcy for Profit”). They concluded the article with this paragraph in order to give it special emphasis.

The National Commission on Financial Institution Reform, Recovery and Enforcement (NCFIRRE) investigated the causes of the savings and loan debacle that Akerlof and Romer referenced.

The Financial Crisis Inquiry Commission (FCIC) investigated the causes of the current U.S. crisis. It reported:

The “race to the weakest supervisor” did not occur only within the U.S. Brooksley Born and a former senior SEC official have confirmed to me that UK regulators directly pitched U.S. financial firms to relocate operations to the City of London in order to obtain weaker supervision. “Fed lite” supervision was a competitive response to the FSA’s “reg lite” system of deliberately weak supervision. The City of London became the most criminogenic environment in the world for financial fraud, which is why so many UK banks and units of foreign banks located in the City have caused the major scandals in the UK and globally.

The investigations into the Irish crisis described their deliberately weak supervision as an EU policy.

Only Regulators and Prosecutors can Break a Gresham’s Dynamic and Save Markets

In its 2011-2012 Global Competiveness Report, the WEF conceded that effective financial regulation is essential to a safe and sound financial system.

The key potential of regulators and prosecutors is that we are not employees or agents of the banks we regulate. Control frauds use their powers to hire, fire, promote, and compensate to suborn the supposed internal and external “controls” (such as auditors). As Akerlof and Romer noted, accounting control fraud is a “sure thing” that will promptly produce record (albeit fictional) profits. Creditors love to lend to highly profitable borrowers. Private markets do not “discipline” accounting control frauds – they fund their rapid expansion.

Control frauds have shown strong abilities to suborn even elite financial players, such as audit partners at top tier firms. George Akerlof was the first economist to apply the concept of Gresham’s law as a metaphor to explain how control fraud can create a competitive advantage that drives honest firms out of the markets. In his famous article on markets for “lemons” he explained.

Effective financial regulation is not the enemy of markets or competition – it is essential to the preservation of well-functioning markets and the ability of honest business people to compete. Control fraud begets fraud in the industry and other professions that are supposed to serve as controls. NCFIRRE found that:

Modern Executive Compensation is Criminogenic

In a delicious irony, Business Week asked Franklin Raines, Fannie Mae’s CEO why there was such widespread securities fraud during the Enron-era. Raines replied:

The WEF is, again, a force for harm. It has an index for performance pay. CEOs who participate in the WEF survey are instructed that tying pay to performance is a desirable step, but there is no attempt by the WEF to verify that the dominant executive compensation system in their Nation is tied to long-term performance and has claw-back rights. The index, therefore, tells Nations that they should make their financial environments even more criminogenic.

The WEF Gets it so Wrong Because it Ignores Accounting Control Frauds

WEF’s competitiveness index has a series of indices that relate to the financial system and the quality of public and private institutions. The WEF loved Ireland, Iceland, and the UK’s financial systems while they were massively insolvent – an insolvency hid by accounting fraud and the grotesque failure of EU Nations and audit bodies to interpret international accounting standards as requiring lenders to recognize losses arising from their fraudulent lending.

In its 2006-2007 and 2007-2008 GCI’s, WEF’s executive survey claimed that Irish banks’ “soundness” was, respectively, the 3rd and 5th best in the world. Today, the same index rates them 144 – the worst in the world. The truth is that the worst Irish banks were in economic reality insolvent long before 2006 because of their fraudulent lending practices.

The respective ranks WEF gave Iceland’s banks in those years were 26 and 29. The WEF now ranks them 136. Spain’s banks are down to 109th from 16 and 19. The UK’s banks fell from the fiction that they were the best in the world (2006-07) (4th best in 2007-2008) to 97.

The WEF’s Global Risk Reports’ financial warnings are every bit as embarrassing. They are overwhelmingly odes to the austerity that threw the Eurozone back into a gratuitous recession.

The WEF survey is a mass of business prejudices collated and called science. If the CEOs, despite their close ties with the banks (indeed, many of them are bankers) cannot even spot the problems of banks in Ireland, Iceland, the UK, and Spain over a year after the bubbles have ceased expanding they are even more useless than scholars feared. It is time for WEF to get out of the business of being an apologist for and enabler of control fraud and to tell the likes of Goldman Sachs that a banker who sells its clients toxic mortgages the bank describe internally as “shitty” is a bank that is degrading the state of the world and it is unwelcome in Davos.

Exhibit A

The Faces of Desupervision in the U.S.: “Chainsaw” Gilleran and friends – America’s leading bank lobbyists act together with their faux regulators to destroy effective regulation and supervision.

Source

The ability of the SDIs to commit fraud with impunity from the criminal laws is a defining element of crony capitalism. The impunity and implicit national subsidies to SDIs combine to make “free markets” an oxymoron. The SDIs’ economic power translates easily into dominant political power. Crony capitalism cripples markets and democracy.

The ability of the SDIs’ senior officers to commit massive frauds with impunity from the criminal laws makes “control fraud” a “sure thing.” Control fraud will make the largest banks’ senior officers exceptionally wealthy very quickly – but it will also cause severe harm to the public (and often the bank). Control fraud occurs when the persons who control a seemingly legitimate entity use it as a “weapon” to defraud. In finance, accounting is the “weapon of choice.” It is important to remember, however, that other forms of control fraud maim and kill hundreds of thousands and cause grave environmental damage. We must always remember the infant formula scandal in China where 300,000 infants were hospitalized with kidney stones due to consumer frauds that drove every honest manufacturer out of business.

Large, individual accounting control frauds cause greater financial losses than all other forms of property crime – combined. Accounting control frauds are weapons of mass financial destruction. Epidemics of accounting control fraud drove the national crises that produced the Great Recession. We have reliable information on this in the United States, the United Kingdom, Ireland, and Iceland. Spain has kept the facts about lending too opaque to determine reliably what caused their bubble to hyper-inflate, but the lending pattern is consistent with accounting control fraud. These accounting control fraud epidemics drove crises that caused a loss of over $20 trillion in wealth and cost roughly 20 million workers their jobs.

These epidemics of accounting control fraud were not random “black swan” events. Criminogenic environments produce such intense and perverse incentives that they generate epidemics of control fraud. Our financial policies have been so criminogenic for decades that we are suffering recurrent, intensifying financial crises. WEF is one of the important architects and engineers that have made our financial system so criminogenic. WEF’s dogmas and policies are so perverse that they drive financial crises, create crony capitalism, and make WEF’s leading products (the Global Competitiveness Index (GCI) and Global Risk Reports (GRR) epic embarrassments. The WEF is degrading the state of the world.

Criminogenic environments for Accounting Control Fraud

1. The dogma that control fraud cannot be materialEach of these factors need not be present. I discuss here only the first three environmental characteristics, which are the most important.

2. The three “de’s” – deregulation, desupervision, and de facto decriminalization

3. Modern executive and professional compensation

4. The ability to grow quickly

5. Extreme leverage

6. Ease of entry

7. Assets that lack readily verifiable market values

8. Weak accounting requirements, particularly on allowances for loan and lease losses (ALLL)

9. Distressed banks

Fraud Deniers

In 2012, in response to endemic, elite financial frauds, the WEF declared the following without citation or reasoning in its 2012 report on “Rethinking Financial Innovation.”

6.1.1 Consumer DisserviceThis is a convenient dogma for a group of CEOs to hold. It is an empirical claim that is falsified by reality, but it is a vital belief if one is a philosophical opponent of regulation. Alan Greenspan was the high priest of this dogma, claiming that there was no such thing as an unregulated market because private creditors always regulated markets to prevent misconduct. Greenspan’s most infamous statement of this dogma was to Brooksley Born, then Chair of the Commodities Futures Trading Commission in connection with her proposal to investigate whether to regulate credit default swaps (CDS). Here is her account of the discussion.

Malfeasance and outright fraud [in finance] are extraordinarily damaging but also, fortunately, extremely rare.

“Well, Brooksley, I guess you and I will never agree about fraud” [Greenspan]Greenspan later admitted that this dogma had failed. The WEF has, recurrently (and implicitly) assumed away control fraud because it shares Greenspan’s dogma. (The implicit nature of the assumption is particularly dangerous – and symptomatic of dogma. It is the things we assume out of existence implicitly that are most dangerous because we do not consciously know we have made the assumption and therefore never test its accuracy.)

“What is there not to agree on?” [Born]

“Well, you probably will always believe there should be laws against fraud, and I don’t think there is any need for a law against fraud,” she recalls. Greenspan, Born says, believed the market would take care of itself.

The leading “law and economics” text on corporate law has taught a generation of American lawyers that “a rule against fraud is not an essential or … an important ingredient of securities markets” (Easterbrook & Fischel 1991).

WEF’s founding ideology is “stakeholder” theory – the philosophical belief that a corporation should serve the interests of its stakeholders. The stakeholders include stockholders, creditors, and workers. Variants of control fraud target each of these stakeholders. Control frauds, therefore, are the kryptonite to stakeholder theory. Control frauds drive stakes through their stakeholders. WEF’s solution is to assume away reality. WEF ignores the findings about control fraud made by modern criminology, effective regulators and prosecutors, and top economists and to embrace Greenspan’s dogma even after Greenspan has abandoned it.

I cite information below on the dominant role of fraud during the savings and loan debacle. The role of accounting control fraud in the Enron-era is not in dispute. My FCIC testimony details the extraordinary levels of accounting control fraud driving the U.S. crisis. (I have other papers discussing the decisive role of accounting control fraud in Ireland and Iceland.) The briefest version is that by 2006, roughly 40% of mortgage loans made that year were “liar’s” loans. The incidence of fraud in liar’s loans is 90%. Lenders put the lies in liar’s loans.

The figure for liar’s loans was even higher in the UK. On January 25, 2012, Martin Wheatley delivered a speech to the British Bankers’ Association entitled “My Vision for the FCA.”

And so it must be different from some of the behaviour we saw during the boom years for the housing market.

Here we saw many examples of both poor lending and poor borrowing. It became more common for people to borrow without having their income verified – 45% of people did this at the market’s peak – and, as many have observed, both lenders and consumers were caught up in a misplaced faith in never-ending house price rises.

It is now obvious that the market in the years leading up to the crisis was unsustainable. The crisis and its aftermath changed things temporarily, but we want to change things for the better, for good.

And so here we have to look at the FSA’s mortgage market review proposals, these are currently out for consultation; we hope to be able to finalise rules in the summer.

And what our first-time buyer won’t see in a FCA-regulated world is a queue of lenders waiting to offer them a loan on the basis of what they claim their income is, with no proof required.

And they won’t find brokers thinking they can get away with persuading them to lie about their income.

This is why, based on our discussions with you, with brokers, and with consumer organisations, we are embedding common sense standards to lending across the board, so that we don’t see a return to the risky mortgage lending and borrowing seen in the boom times.Forty-five percent of the home mortgage loans in the UK were liar’s loans – and the new “supervisor” believes that the bank officers made these loans because they all went simultaneously delusional and believed that there was an infinite bubble.

The Three “De’s” and the First Virgin Crisis

George Akerlof was made the Nobel Laureate in Economics in 2001. He co-authored a famous article in 1993 about accounting control fraud (“Looting: the Economic Underworld of Bankruptcy for Profit”). They concluded the article with this paragraph in order to give it special emphasis.

Neither the public nor economists foresaw that [S&L deregulation was] bound to produce looting. Nor, unaware of the concept, could they have known how serious it would be. Thus the regulators in the field who understood what was happening from the beginning found lukewarm support, at best, for their cause. Now we know better. If we learn from experience, history need not repeat itself (George Akerlof & Paul Romer.1993: 60).Akerlof & Romer explained why deregulation encouraged control fraud.

[M]any economists still seem not to understand that a combination of circumstances in the 1980s made it very easy to loot a financial institution with little risk of prosecution. Once this is clear, it becomes obvious that high-risk strategies that would pay off only in some states of the world were only for the timid. Why abuse the system to pursue a gamble that might pay off when you can exploit a sure thing with little risk of prosecution? (Akerlof & Romer 1993: 4-5).N. Gregory Mankiw was a discussant on the Akerlof & Romer paper. His infamous response to their warning about control fraud was that: “it would be irrational for savings and loans [CEOs] not to loot.” Mankiw is arguably the most influential economist because of his textbook and his role as a leading Republican economic adviser. “Mankiw morality” explains why theoclassical economics fails substantively and ethically.

The National Commission on Financial Institution Reform, Recovery and Enforcement (NCFIRRE) investigated the causes of the savings and loan debacle that Akerlof and Romer referenced.

The typical large failure [grew] at an extremely rapid rate, achieving high concentrations of assets in risky ventures…. [E]very accounting trick available was used…. Evidence of fraud was invariably present as was the ability of the operators to “milk” the organization (NCFIRRE 1993).Investigations, and successful actions and prosecutions, by regulators, the FBI, prosecutors, and white-collar criminologists confirmed the key role that accounting control fraud played in causing the second phase of the S&L debacle.

The Financial Crisis Inquiry Commission (FCIC) investigated the causes of the current U.S. crisis. It reported:

We conclude widespread failures in financial regulation and supervision proved devastating to the stability of the nation’s financial markets. The sentries were not at their posts …due to the widely accepted faith in the self-correcting nature of the markets and the ability of financial institutions to effectively police themselves.

More than 30 years of deregulation and reliance on self-regulation

… championed by …Greenspan and others, supported by successive administrations and Congresses, and actively pushed by the powerful financial industry … stripped away key safeguards, which could have helped avoid catastrophe.

This approach had opened up gaps in oversight of critical are as with trillions of dollars at risk….

In addition, the government permitted financial firms to pick their preferred regulators in what became a race to the weakest supervisor.” [FCIC Report:xviii]The Office of Thrift Supervision (OTS) “won” the U.S. race to the bottom. The photograph of OTS head “Chainsaw” Gilleran (see Exhibit A at the end of this text) is the iconic image of this crisis. It was intended to symbolize that the regulator (sic) and the industry would work together to destroy any regulations or supervision the industry felt was onerous. The OTS and the FDIC were so proud of the image that they placed it in the annual report of the FDIC.

The “race to the weakest supervisor” did not occur only within the U.S. Brooksley Born and a former senior SEC official have confirmed to me that UK regulators directly pitched U.S. financial firms to relocate operations to the City of London in order to obtain weaker supervision. “Fed lite” supervision was a competitive response to the FSA’s “reg lite” system of deliberately weak supervision. The City of London became the most criminogenic environment in the world for financial fraud, which is why so many UK banks and units of foreign banks located in the City have caused the major scandals in the UK and globally.

The investigations into the Irish crisis described their deliberately weak supervision as an EU policy.

…there was a socio-political context in which it would have taken some courage to seem to prick the Irish property bubble….

generic weaknesses in [EU] regulation and supervision…

Four main failings of supervision: (i) Supervisory culture was insufficiently intrusive, and staff resources were seriously inadequate ….

On-site inspections were infrequent. Supervisors … imposed no penalties on banks at all….The FCIC dissent claimed that deregulation and desupervision could not be a major cause of the U.S. crisis because the crisis also occurred in Europe. The dissent incorrectly (and implicitly) assumed that the three de’s did not occur in the EU.

Ireland’s mounting financial vulnerabilities meant that strong action was called for to over-ride the prevalent light-touch and market-driven fashions of supervision: to call a spade a spade….

failure to identify, recognise the gravity of, and take tough remedial action to correct such serious governance breaches was a cardinal error of supervision…. [Report on the Irish Crisis (2010)].

Only Regulators and Prosecutors can Break a Gresham’s Dynamic and Save Markets

In its 2011-2012 Global Competiveness Report, the WEF conceded that effective financial regulation is essential to a safe and sound financial system.

In order to fulfill all those functions, the banking sector needs to be trustworthy and transparent, and—as has been made so clear recently—financial markets need appropriate regulation to protect investors and other actors in the economy at large [p. 7].Its GCI, however, has no index category for effective financial regulation – only securities law regulation. The WEF has several more general indices that refer to regulation. Each of them assumes that regulation is inherently harmful – rather than essential. The WEF encourages Nations to use its indices to engage in a competition in regulatory laxity. It makes the financial environment deeply criminogenic.

The key potential of regulators and prosecutors is that we are not employees or agents of the banks we regulate. Control frauds use their powers to hire, fire, promote, and compensate to suborn the supposed internal and external “controls” (such as auditors). As Akerlof and Romer noted, accounting control fraud is a “sure thing” that will promptly produce record (albeit fictional) profits. Creditors love to lend to highly profitable borrowers. Private markets do not “discipline” accounting control frauds – they fund their rapid expansion.

Control frauds have shown strong abilities to suborn even elite financial players, such as audit partners at top tier firms. George Akerlof was the first economist to apply the concept of Gresham’s law as a metaphor to explain how control fraud can create a competitive advantage that drives honest firms out of the markets. In his famous article on markets for “lemons” he explained.

[D]ishonest dealings tend to drive honest dealings out of the market. The cost of dishonesty, therefore, lies not only in the amount by which the purchaser is cheated; the cost also must include the loss incurred from driving legitimate business out of existence. George Akerlof (1970).While economists have had no excuse for not understanding this dynamic for over 40 years, economists were not the first to explain a Gresham’s dynamic. An acute observer of human nature wrote centuries earlier than Akerlof:

The Lilliputians look upon fraud as a greater crime than theft. For, they allege, care and vigilance, with a very common understanding, can protect a man’s goods from thieves, but honesty hath no fence against superior cunning. . . where fraud is permitted or connived at, or hath no law to punish it, the honest dealer is always undone, and the knave gets the advantage. [Swift, J. Gulliver’s Travels].The WEF, through its many indices that purport to measure internal and external controls and quality of governance spreads the false belief that these actions prevent accounting control fraud. A recent OECD report confirms that the EU suffered from the complete failure of audit and governance to prevent the crisis.

Effective financial regulation is not the enemy of markets or competition – it is essential to the preservation of well-functioning markets and the ability of honest business people to compete. Control fraud begets fraud in the industry and other professions that are supposed to serve as controls. NCFIRRE found that:

abusive operators of S&L[s] sought out compliant and cooperative accountants. The result was a sort of “Gresham’s Law” in which the bad professionals forced out the good (NCFIRRE 1993).FCIC found a similar Gresham’s dynamic among appraisers.

From 2000 to 2007, a coalition of appraisal organizations … delivered to Washington officials a public petition; signed by 11,000 appraisers…. [I]t charged that lenders were pressuring appraisers to place artificially high prices on properties [and] “blacklisting honest appraisers” and instead assigning business only to appraisers who would hit the desired price targets.( FCIC: 18)Note that loan origination fraud originated with the loan originators rather than the borrowers.

Modern Executive Compensation is Criminogenic

In a delicious irony, Business Week asked Franklin Raines, Fannie Mae’s CEO why there was such widespread securities fraud during the Enron-era. Raines replied:

Don’t just say: “If you hit this revenue number, your bonus is going to be this.” It sets up an incentive that’s overwhelming. You wave enough money in front of people, and good people will do bad things.Raines knew that bonuses had corrupted the unit at Fannie that should have been most resistant – internal audit. We know that Raines read Rajappa’s speech because he made handwritten comments on it suggesting how to strengthen the message, which he returned to Rajappa.

“By now every one of you must have 6.46 [EPS] branded in your brains. You must be able to say it in your sleep, you must be able to recite it forwards and backwards, you must have a raging fire in your belly that burns away all doubts, you must live, breath and dream 6.46, you must be obsessed on 6.46…. After all, thanks to Frank, we all have a lot of money riding on it…. We must do this with a fiery determination, not on some days, not on most days but day in and day out, give it your best, not 50%, not 75%, not 100%, but 150%.The investigation into the Irish crisis by Mr. Nyberg displays poor analytics, but the facts he found demonstrate the perverse effects of compensation in encouraging accounting control fraud and enlisting the support of subordinates.

Remember, Frank has given us an opportunity to earn not just our salaries, benefits, raises, ESPP, but substantially over and above if we make 6.46. So it is our moral obligation to give well above our 100% and if we do this, we would have made tangible contributions to Frank’s goals.” (Mr. Rajappa, head of Fannie’s internal audit, emphasis in original.)

Targets that were intended to be demanding through the pursuit of sound policies and prudent spread of risk were easily achieved through volume lending to the property sector. (Nyberg 2011: 30)The last sentence makes explicit the root ethical issue. FCIC examined the same question.

Bank management and boards in some of the other covered banks feared that, if they did not yield to the pressure to be as profitable as Anglo, in particular, they would face loss of long-standing customers, declining bank value, potential takeover and a loss of professional respect. (Nyberg 2011: v)

The [compensation] models, as operated by the covered banks in Ireland, lacked effective modifiers for risk. Therefore rapid loan asset growth was extensively and significantly rewarded at executive and other senior levels in most banks, and to a lesser extent among staff where profit sharing and/or share ownership schemes existed.” (Nyberg 2011: 30)

“The associated risks appeared relevant to management and boards only to the extent that growth targets were not seriously compromised. (Nyberg 2011: 49)

Occasionally, management and boards clearly mandated changes to credit criteria. However, in most banks, changes just steadily evolved to enable earnings growth targets to be met by increased lending. (Nyberg 2011: 34)

all of the covered banks regularly and materially deviated from their formal policies in order to facilitate rapid and significant property lending growth. In some banks, credit policies were revised to accommodate exceptions, to be followed by further exceptions to this new policy, thereby continuing the cycle. (Nyberg 2011).

The demand for Development Finance was so strong over the Period that bank and individual growth targets were easily met from this sector. Both of the bigger banks continued to lend into the more speculative parts of the property market well into 2008, even though demand for residential property (a major end-user) had begun to decline by the end of 2006. (Nyberg 2011: 35-36)

The few that admitted to feeling any degree of concern at the change of strategy often added that consistent opposition would probably have meant formal or informal sanctioning (Nyberg 2011: v).

We conclude there was a systemic breakdown in accountability and ethics. The integrity of our financial markets and the public’s trust in those markets are essential to the economic well-being of our nation.Modern executive compensation further misaligns executives’ financial interests with the shareholders’. It is, instead, superb for fraud because it is very large, largely based on short-term reported earnings or share prices (which the CEO can easily manipulate), and lacks a “claw back” provision. It helps fraudulent CEOs convert firm assets to his personal benefit through seemingly normal corporate mechanisms, which makes it harder to prosecute.

The WEF is, again, a force for harm. It has an index for performance pay. CEOs who participate in the WEF survey are instructed that tying pay to performance is a desirable step, but there is no attempt by the WEF to verify that the dominant executive compensation system in their Nation is tied to long-term performance and has claw-back rights. The index, therefore, tells Nations that they should make their financial environments even more criminogenic.

The WEF Gets it so Wrong Because it Ignores Accounting Control Frauds

WEF’s competitiveness index has a series of indices that relate to the financial system and the quality of public and private institutions. The WEF loved Ireland, Iceland, and the UK’s financial systems while they were massively insolvent – an insolvency hid by accounting fraud and the grotesque failure of EU Nations and audit bodies to interpret international accounting standards as requiring lenders to recognize losses arising from their fraudulent lending.

In its 2006-2007 and 2007-2008 GCI’s, WEF’s executive survey claimed that Irish banks’ “soundness” was, respectively, the 3rd and 5th best in the world. Today, the same index rates them 144 – the worst in the world. The truth is that the worst Irish banks were in economic reality insolvent long before 2006 because of their fraudulent lending practices.

The respective ranks WEF gave Iceland’s banks in those years were 26 and 29. The WEF now ranks them 136. Spain’s banks are down to 109th from 16 and 19. The UK’s banks fell from the fiction that they were the best in the world (2006-07) (4th best in 2007-2008) to 97.

The WEF’s Global Risk Reports’ financial warnings are every bit as embarrassing. They are overwhelmingly odes to the austerity that threw the Eurozone back into a gratuitous recession.

The WEF survey is a mass of business prejudices collated and called science. If the CEOs, despite their close ties with the banks (indeed, many of them are bankers) cannot even spot the problems of banks in Ireland, Iceland, the UK, and Spain over a year after the bubbles have ceased expanding they are even more useless than scholars feared. It is time for WEF to get out of the business of being an apologist for and enabler of control fraud and to tell the likes of Goldman Sachs that a banker who sells its clients toxic mortgages the bank describe internally as “shitty” is a bank that is degrading the state of the world and it is unwelcome in Davos.

Exhibit A

The Faces of Desupervision in the U.S.: “Chainsaw” Gilleran and friends – America’s leading bank lobbyists act together with their faux regulators to destroy effective regulation and supervision.

Source

Fed's Balance Sheet Tops $3 Trillion, But...

... that's not true. The Fed's balance sheet, from a transaction basis, topped $3 trillion some 5-6 weeks ago. The only reason the Fed reported a $3 trillion number in today's H.4.1, or $3.013,333 trillion to be precise, is because all those MBS purchased in September and October following the September 13 reactivation of QE4EVA finally settled. In reality, the Fed's balance sheet is now some $3.12 trillion as there is about a $80-$120 billion lag between what the Fed has actually purchased, and what has settled. Luckily, at least Treasury purchases take far less to settle.

None of the above should come as a surprise to anyone: the Fed's balance sheet has been, even purely nominally, at $2.8/2.9 trillion for months. Wake us up when the Fed's balance sheet is $4 trillion, in precisely 11 months.

None of the above should come as a surprise to anyone: the Fed's balance sheet has been, even purely nominally, at $2.8/2.9 trillion for months. Wake us up when the Fed's balance sheet is $4 trillion, in precisely 11 months.

Does China Plan To Establish “China Cities” And “Special Economic Zones” All Over America?

What in the world is China up to? Over the past several years, the Chinese government and large Chinese corporations (which are often at least partially owned by the government) have been systematically buying up businesses, homes, farmland, real estate, infrastructure and natural resources all over America. In some cases, China appears to be attempting to purchase entire communities in one fell swoop. So why is this happening? Is this some form of "economic colonization" that is taking place? Some have speculated that China may be intending to establish "special economic zones" inside the United States modeled after the very successful Chinese city of Shenzhen. Back in the 1970s, Shenzhen was just a very small fishing village, but now it is a sprawling metropolis of over 14 million people. Initially, these "special economic zones" were only established within China, but now the Chinese government has been buying huge tracts of land in foreign countries such as Nigeria and establishing special economic zones in those nations. So could such a thing actually happen in America? Well, according to Dr. Jerome Corsi, a plan being pushed by the Chinese Central Bank would set up "development zones" in the United States that would allow China to "establish Chinese-owned businesses and bring in its citizens to the U.S. to work." Under the plan, some of the $1.17 trillion that the U.S. owes China would be converted from debt to "equity". As a result, "China would own U.S. businesses, U.S. infrastructure and U.S. high-value land, all with a U.S. government guarantee against loss." Does all of this sound far-fetched? Well, it isn't. In fact, the economic colonization of America is already far more advanced than most Americans would dare to imagine.

So how in the world did we get to this point? A few decades ago, the United States was the unchallenged economic powerhouse of the world and China was essentially a third world country.

So what happened?

Well, we entered into a whole bunch of extremely unfavorable "free trade" agreements, and countries such as China began to aggressively use "free trade" as an economic weapon against us.

Over the past decade, we have lost tens of thousands of businesses and millions of jobs to China.

When the final numbers for 2012 come out, our trade deficit with China for the year will be well over 300 billion dollars, and that will be the largest trade deficit that one country has had with another country in the history of the world.

Overall, the U.S. has run a trade deficit with China over the past decade that comes to more than 2.3 trillion dollars. That 2.3 trillion dollars could have gone to U.S. businesses and U.S. workers, and in turn taxes would have been paid on all of that money. But instead, all of that money went to China.

Rather than just sitting on all of that money, China has been lending much of it back to us - at interest. We now owe China more than a trillion dollars, and our politicians are constantly pleading with China to lend more money to us so that we can finance our exploding debt.

Today, the U.S. government pays China approximately 100 million dollars a day in interest on the debt that we owe them. Those that say that the U.S. debt "does not matter" are being incredibly foolish.

So thanks to our massive trade deficit and our exploding national debt, China is systematically getting wealthier and the United States is systematically getting poorer.

And now China is starting to use a lot of that wealth to aggressively expand their power and influence around the globe.

But isn't it more than a bit far-fetched to suggest that China may be planning to establish Chinese cities and special economic zones in America?

Not really.

Just look at what has already happened up in Canada. It is well-known that the Chinese population of Vancouver, Canada has absolutely exploded in recent years. In fact, the Vancouver suburb of Richmond is now approximately half Chinese. The following is an excerpt from a BBC article...

But in other areas of the United States, the Chinese are approaching things much more systematically.

For example, as I have written about previously, a Chinese group identified as "Sino-Michigan Properties LLC" has purchased 200 acres of land near the town of Milan, Michigan. Their stated goal is to build a "China City" that has artificial lakes, a Chinese cultural center and hundreds of housing units for Chinese citizens.

In other instances, large chunks of real estate in major U.S. cities that are down on their luck are being snapped up by Chinese investors. Just check out what a Fortune article from a while back says has been happening over in Toledo, Ohio...

The Chinese certainly do seem to be laying the groundwork for something. They have been voraciously gobbling up important infrastructure all over the country. The following comes from a recent American Free Press article...

Isn't there a national security risk?

Sadly, there isn't much of anything that our politicians won't sell these days as long as someone is willing to flash a lot of cash.

The Chinese have also been busy buying up important real estate on the east coast as a recent Forbes article explained….

They have also been purchasing rights to vital oil and natural gas deposits all over the United States.

There have been two Chinese companies that have been primarily involved in this effort.

The first is the China National Offshore Oil Corporation (CNOOC). According to Wikipedia, CNOOC is 100 percent owned by the Chinese government…

And as you can see from the following list compiled by the Wall Street Journal, those two companies have been extremely aggressive in buying up rights to oil and natural gas all over the nation...

That is a very good question.

For a nation that purports to be pursuing "energy independence", we sure do have a funny way of going about things.

Unfortunately, the sad truth is that China is absolutely mopping the floor with the United States on the global economic stage. China is rising and America is in an advanced state of decline. Global economic power has shifted dramatically and most Americans still don't understand what has happened.

The following are 44 more signs of how dominant the economy of China has become...

1. A Chinese firm recently made a $2.6 billion offer to buy movie theater chain AMC.

2. A different Chinese firm made a $1.8 billion offer to buy aircraft maker Hawker Beechcraft.

3. In December it was announced that a Chinese group would be purchasing AIG's plane leasing unit for $4.23 billion.

4. It was recently announced that the Federal Reserve will now allow Chinese banks to buy up American banks.

5. A $190 million bridge project up in Alaska was awarded to a Chinese firm.

6. A $400 million contract to renovate the Alexander Hamilton bridge in New York was awarded to a Chinese firm.

7. A $7.2 billion contract to construct a new bridge between San Francisco and Oakland was awarded to a Chinese firm.

8. The uniforms for the U.S. Olympic team were made in China.

9. 85 percent of all artificial Christmas trees are made in China.

10. The new World Trade Center tower is going to include glass that has been imported from China.

11. The new Martin Luther King memorial on the National Mall was made in China.

12. In 2001, American consumers spent 102 billion dollars on products made in China. In 2011, American consumers spent 399 billion dollars on products made in China.

13. The United States spends about 4 dollars on goods and services from China for every one dollar that China spends on goods and services from the United States.

14. According to the New York Times, a Jeep Grand Cherokee that costs $27,490 in the United States costs about $85,000 in China thanks to all the tariffs.

15. The Chinese economy has grown 7 times faster than the U.S. economy has over the past decade.

16. The United States has lost a staggering 32 percent of its manufacturing jobs since the year 2000.

17. The United States has lost an average of 50,000 manufacturing jobs per month since China joined the World Trade Organization in 2001.

18. Overall, the United States has lost a total of more than 56,000 manufacturing facilities since 2001.

19. According to the Economic Policy Institute, America is losing half a million jobs to China every single year.

20. Between December 2000 and December 2010, 38 percent of the manufacturing jobs in Ohio were lost, 42 percent of the manufacturing jobs in North Carolina were lost and 48 percent of the manufacturing jobs in Michigan were lost.

21. In 2010, China produced more than twice as many automobiles as the United States did.

22. Since the auto industry bailout, approximately 70 percent of all GM vehicles have been built outside the United States.

23. After being bailed out by U.S. taxpayers, General Motors is currently involved in 11 joint ventures with companies owned by the Chinese government. The price for entering into many of these “joint ventures” was a transfer of “state of the art technology” from General Motors to the communist Chinese.

24. Back in 1998, the United States had 25 percent of the world’s high-tech export market and China had just 10 percent. Ten years later, the United States had less than 15 percent and China’s share had soared to 20 percent.

25. The United States has lost more than a quarter of all of its high-tech manufacturing jobs over the past ten years.

26. China’s number one export to the U.S. is computer equipment.

27. The number one U.S. export to China is "scrap and trash".

28. The U.S. trade deficit with China is now more than 28 times larger than it was back in 1990.

29. Back in 1985, the U.S. trade deficit with China was just 6 million dollars for the entire year. For the month of November 2012 alone, the U.S. trade deficit with China was 28.9 billion dollars.

30. China now consumes more energy than the United States does.

31. China is now the leading manufacturer of goods in the entire world.

32. China uses more cement than the rest of the world combined.

33. China is now the number one producer of wind and solar power on the entire globe.

34. Today, China produces nearly twice as much beer as the United States does.

35. Right now, China is producing more than three times as much coal as the United States does.

36. China now produces 11 times as much steel as the United States does.

37. China produces more than 90 percent of the global supply of rare earth elements.

38. China is now the number one supplier of components that are critical to the operation of U.S. defense systems.

39. A recent investigation by the U.S. Senate Committee on Armed Services found more than one million counterfeit Chinese parts in the Department of Defense supply chain.

40. 15 years ago, China was 14th in the world in published scientific research articles. But now, China is expected to pass the United States and become number one very shortly.

41. China now awards more doctoral degrees in engineering each year than the United States does.

42. According to one study, the Chinese economy already has roughly the same amount of purchasing power as the U.S. economy does.

43. According to the IMF, China will pass the United States and will become the largest economy in the world in 2016.

44. Nobel economist Robert W. Fogel of the University of Chicago is projecting that the Chinese economy will be three times larger than the U.S. economy by the year 2040 if current trends continue.

Without the "globalization" of the world economy, none of this would have ever happened. But instead of admitting our mistakes and fixing them, our politicians continue to press for even more "free trade" and even more integration with communist nations such as China.

In fact, according to Dr. Jerome Corsi, the U.S. government has already set up 257 "foreign trade zones" all over America. These "foreign trade zones" are apparently given "special U.S. customs treatment" and are used to promote "free trade"…

According to Corsi, a professor of economics at Tsighua University in Beijing named Yu Qiao has suggested the following plan as a way to transform the debt that the United States owes China into something more "tangible"...

In the years ahead, perhaps many of you will end up working in a "special economic zone" for a Chinese company on a project that is being financially guaranteed by the U.S. government.

If that sounds like a form of slavery to you, the truth is that you are probably not too far off the mark.

The borrower is the servant of the lender, and we should have never allowed ourselves to get into so much debt.

Now we will pay the price.

To get an idea of how much the world has changed in recent years, just check out this incredible photo which contrasts the decline of Detroit over the years with the amazing rise of Shanghai, China.

Things did not have to turn out this way. Unfortunately, we made decades of incredibly foolish decisions and we wrecked the greatest economic machine that the world has ever seen.

Now the future for America looks really bleak.

Or could it be that I am being too pessimistic? Please feel free to post a comment with your thoughts below...

So how in the world did we get to this point? A few decades ago, the United States was the unchallenged economic powerhouse of the world and China was essentially a third world country.

So what happened?

Well, we entered into a whole bunch of extremely unfavorable "free trade" agreements, and countries such as China began to aggressively use "free trade" as an economic weapon against us.

Over the past decade, we have lost tens of thousands of businesses and millions of jobs to China.

When the final numbers for 2012 come out, our trade deficit with China for the year will be well over 300 billion dollars, and that will be the largest trade deficit that one country has had with another country in the history of the world.

Overall, the U.S. has run a trade deficit with China over the past decade that comes to more than 2.3 trillion dollars. That 2.3 trillion dollars could have gone to U.S. businesses and U.S. workers, and in turn taxes would have been paid on all of that money. But instead, all of that money went to China.

Rather than just sitting on all of that money, China has been lending much of it back to us - at interest. We now owe China more than a trillion dollars, and our politicians are constantly pleading with China to lend more money to us so that we can finance our exploding debt.

Today, the U.S. government pays China approximately 100 million dollars a day in interest on the debt that we owe them. Those that say that the U.S. debt "does not matter" are being incredibly foolish.

So thanks to our massive trade deficit and our exploding national debt, China is systematically getting wealthier and the United States is systematically getting poorer.

And now China is starting to use a lot of that wealth to aggressively expand their power and influence around the globe.

But isn't it more than a bit far-fetched to suggest that China may be planning to establish Chinese cities and special economic zones in America?

Not really.

Just look at what has already happened up in Canada. It is well-known that the Chinese population of Vancouver, Canada has absolutely exploded in recent years. In fact, the Vancouver suburb of Richmond is now approximately half Chinese. The following is an excerpt from a BBC article...

Richmond is North America's most Asian city - 50% of residents here identify themselves as Chinese. But it's not just here that the Chinese community in British Columbia (BC) - some 407,000 strong - has left its mark. All across Vancouver, Chinese-Canadians have helped shape the local landscape.A similar thing is happening in many communities along the west coast of the United States. In fact, Chinese citizens purchased one out of every ten homes that were sold in the state of California in 2011.

But in other areas of the United States, the Chinese are approaching things much more systematically.

For example, as I have written about previously, a Chinese group identified as "Sino-Michigan Properties LLC" has purchased 200 acres of land near the town of Milan, Michigan. Their stated goal is to build a "China City" that has artificial lakes, a Chinese cultural center and hundreds of housing units for Chinese citizens.

In other instances, large chunks of real estate in major U.S. cities that are down on their luck are being snapped up by Chinese investors. Just check out what a Fortune article from a while back says has been happening over in Toledo, Ohio...

In March 2011, Chinese investors paid $2.15 million cash for a restaurant complex on the Maumee River in Toledo, Ohio. Soon they put down another $3.8 million on 69 acres of newly decontaminated land in the city's Marina District, promising to invest $200 million in a new residential-commercial development. That September, another Chinese firm spent $3 million for an aging hotel across a nearby bridge with a view of the minor league ballpark.Toledo is being promoted to Chinese investors as a "5-star logistics region". From Toledo it is very easy to get to Chicago, Detroit, Cleveland, Pittsburgh, Columbus and Indianapolis...

With a population of 287,000, Toledo is only the fourth largest city in Ohio, but it lies at the junction of two important highways -- I-75 and I-80/90. "My vision is to make Toledo a true international city," Toledo's Mayor Mike Bell told the Toledo Blade.But some of these deals appear to be about far more than just making "investments". According to the Idaho Statesman, a Chinese company known as Sinomach (which is actually controlled by the Chinese government) was actually interested in developing a 50 square mile self-sustaining "technology zone" south of the Boise airport...

A Chinese national company is interested in developing a 10,000- to 30,000-acre technology zone for industry, retail centers and homes south of the Boise Airport.